Shaping a world where people and communities thrive, Australia and New Zealand Banking Group (ANZ Bank) is a dominant player in the banking industry. Not only is ANZ one of Australia’s big 4 banks but it also features in the esteemed list of the world’s top 50 banks.

Established as Bank of Australasia in 1835 and boasting a rich and illustrious history of over 180 years, ANZ now operates in 34 countries, providing an array of banking and financial products and services to retail, commercial, and institutional customers around the globe.

Here’s a look at the performance of ANZ Bank in 2021:

- Operating income of 17.4 billion

- Profit of $6.2 billion

- Total assets worth $978.9 billion

- 4,0211 total employees

- Share price as of December 2021: $27.5

Now let's delve a little further to learn more about Australia and New Zealand Banking Group’s origins and evolution, right from the time it was established in the nineteenth century to today—just around two centuries later.

Early Beginnings

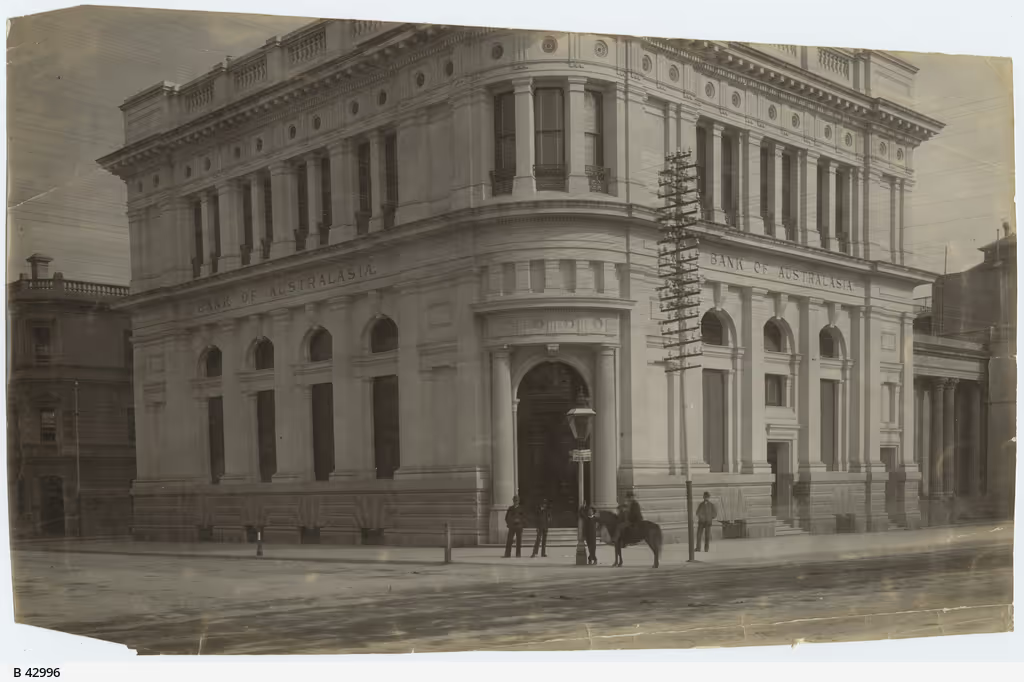

ANZ's forerunner, the Bank of Australasia, was founded in 1835, but efforts to establish it date back to 1832. This was when the Sydney media reported on plans for a "Bank and Whaling Company on the Scotch principle."

However, the whaling idea was dropped in favor of establishing a Royal Bank of Australasia and South Africa. The company would function under a Royal charter obtained from the British Treasury in May 1833, limiting the owners' liability to twice the amount of their shareholding.

On April 1, 1833, the British Treasury issued new rules for applicants for colonial banking charters. The directors were able to begin operations after receiving the charter, and they deployed their staff to Australia on July 10, 1835.

Later, the business of Cornwall Bank was acquired, and offices of Bank of Australasia were opened in Sydney and Hobart in December and Launceston in January 1836. Sydney was assigned as the headquarters.

How AMZ Bank’s Key Predecessor Banks Came Into Being

In July 1837, a resolution was taken in London to establish The Union Bank of Australasia. A struggling Australian bank in Tasmania, Tamar Bank, went to London in quest of investment and discovered a group of investors willing to fund a bank in the colony. These investors established the Union Bank of Australasia, which took over the Tamar Bank and began operations. However, it was renamed The Union Bank of Australia following concerns from the Bank of Australasia over the similarity of names. Unlike the Bank of Australasia, the Union Bank was a joint-stock company with unlimited liability. It continued to trade as such until it was registered under the English Companies Act in 1880.

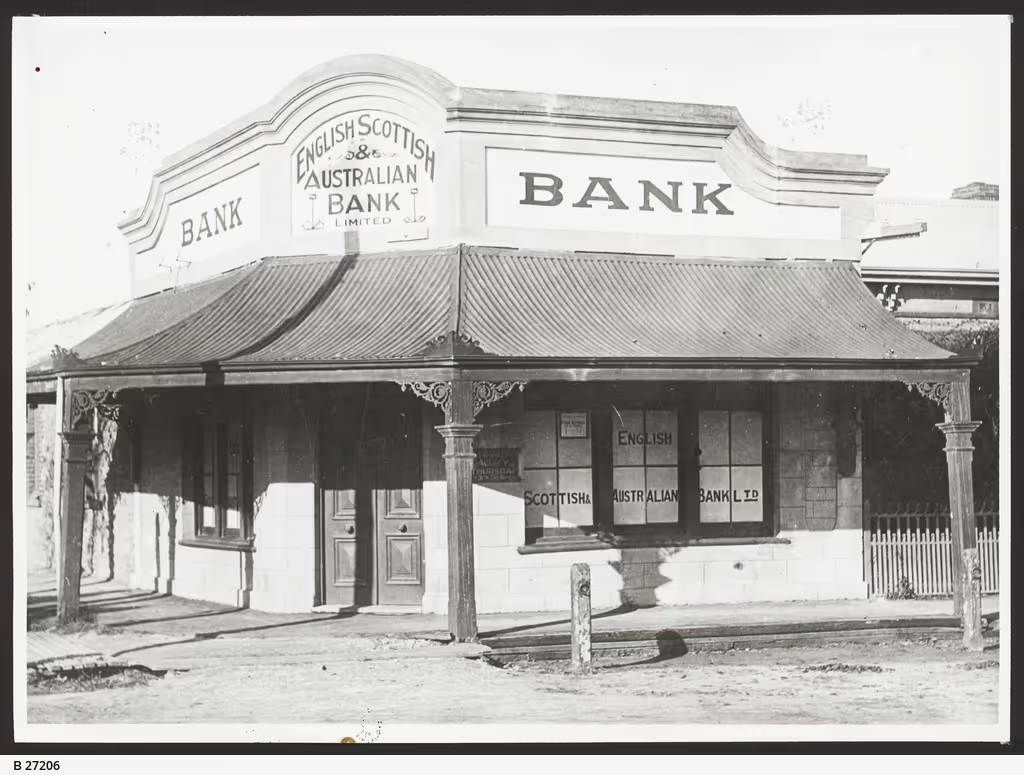

Fast-forward to the 1850s, South Australia saw a general boom due to new copper discoveries. With the rush of new mining customers looking for mortgages, gold and foreign-exchange dealing became key banking services, and branch-banking systems flourished. During this "golden decade," the English, Scottish, and Australian Bank (ES&A) was created in 1852.

The Great 19th Century Banking Crash Hits Australia

Between 1860 and 1890, Australia witnessed economic growth. However, in the late 1880s, the Bank of Australasia and Union Bank began to plan for the impending economic downturn after the prolonged boom. Sure enough, the downturn came, and only 6 of the 28 colonial banks in Australia survived until the end of the century.

The Australasia and Union Bank, on the other hand, had steadily built up cash reserves of up to 20% of all public liabilities. Furthermore, it had considerable floating advances to the money market and a diverse portfolio of gilt-edged equities from which it might draw in an emergency.

Aside from that, the banks had several informal links with other financial institutions. As a result, during the banking crisis of 1893, the Union Bank and the Bank of Australasia had several options to look for assistance, including the Bank of England.

Many post-1850 banks failed because they were governed by over-optimism and a voracious hunt for business with insufficient regard for security. They built branch banks in small towns without carefully weighing the costs and aimed to expand their loan portfolios rapidly.

The Australasia and Union Bank, on the contrary, were careful about opening new offices and accepting loans. With the end of the banking crisis, both the banks attempted to boost their dwindling earnings.

Except in Western Australia, where gold discoveries promised huge potential, salaries were lowered, and marginal branch banks were shuttered. Most importantly, the banks attempted to limit the unprofitable buildup of deposits by decreasing interest rates.

The Union Bank and Bank of Australasia believed that marketing lower-cost loans to customers would lower the cost of funding while also increasing their revenues. In 1895, they reduced interest rates throughout the colonies to 3%, even though other banks did not follow suit.

Growth in the Early Twentieth Century

By 1900, the Bank of Australasia had 12.7% of all deposits and 9.3% of all advances in Australia, whereas the Union held 12.1% and 10.6%, respectively. Both were also members of Australian banking's Big Four banks. This reflects that towards the start of the 20th century, the banks enjoyed relative strength across the Australian Commonwealth. As the Australian economy stabilized, it prompted the banks to pursue “complacent expansion” strategies through branch expansions. Between 1900 and the onset of World War I, the Union Bank opened 100 branches while the Bank of Australasia opened 73 branches.

However, their competitors, who were still reeling from the effects of the 1983 financial crisis, had to worry about reconstruction commitments; their small size and unstable conditions necessitated a mergers and absorption strategy rather than branch banking to ensure market dominance.

The banking systems that existed in 1914 were cemented as a result of World War I. Even so, after the war, rivals of the Union and Australasia bank began to merge to become more competitive, lowering the number of Australian trading banks from 20 to 9.

.avif)

Later, the ES&A also amalgamated with three other banks: the Commercial Bank of Tasmania in 1921, the London Chartered Bank of Australia in 1921, and the Royal Bank of Australia in 1927. Although it may have profited from mergers with banks in places where it was weak, like Tasmania, the Union stuck to its conservative policies and stuck with branch expansions. Between 1918 and 1929, the Union continued to build its branch banking network in an attempt to offset its competitors' rising advantages, opening 41 branches.

Key Takeaway 1: Embrace A Specific Vision

By the 20th century, it became evident that two banks stood out more than most: The Union Bank of Australia and the Bank of Australasia. Starting from scratch in the 1800s, these banks continued to evolve and thrive throughout the century. They displayed incredible foresight and resilience, especially during the banking crisis of 1893.

Indeed, the predecessors of ANZ weathered some of the darkest and most terrible times, with their doors remaining open during depressions, wars, floods, and fires.

Not only this, both the banks earned the prestige of being a part of the top 4 Australian Banks while the other banks still struggled to recover their losses. The Union Bank and Australasia bank remained undefeated due to their excellent management and leadership as well as their ability to analyze different circumstances.

ANZ Begins And Expands Through the 1950s—1980s

During the 1930s, there was considerable discussion about a union between Australasia and the Union Bank, but it wasn't until 1943 that genuine interest in the proposal materialized. Other Australian banks approached both Australasia and the Union as potential partners. However, both saw the other as the most natural choice for a merger.

Both banks were less than half the size of the Bank of New South Wales, the country's largest bank at the time. They both felt that a merger would increase their competitiveness, and it appeared that if they did not act, they would be left behind as their smaller competitors merged.

Furthermore, both were English firms with headquarters in London and had a majority of English stockholders. Their business scales and styles were also quite alike. The Union's strength in pastoral trade supplemented Australasia's economic and industrial field.

Thus, in 1946, lawyers began working on the specifics of a merger in which Bank of Australasia took over the Union’s business. However, it was later determined that the original merger proposal was too costly.

A group of influential Union executives began to resist being taken over by Australasia, believing that the banks were equals and should unite as such. The idea was to establish a new corporation, Australia and New Zealand Bank Limited, which would take over both the Australasia and the Union banks. Finally, on October 1, 1951, ANZ Bank opened its doors.

Promised Success?

ANZ Bank had catapulted to the top tier of banks in Australia and New Zealand after the merger of Australasia and Union. Unfortunately, ANZ’s size did not translate into increased profitability. What went wrong? The government imposed a stringent liquidity requirement, which in effect stipulated that only liquid assets and government securities held in Australia would be counted. When the new convention began, ANZ had more than half of its liquid assets and government securities held outside Australia.

Ultimately, the bank had to reduce lending to meet the required level of liquid assets, which was a setback for ANZ after the merger. To make up for the lost loan business, ANZ Bank began exploring new ways to increase profits and save costs.

In 1956 the ANZ Bank decided to form Australia and New Zealand Savings Bank Limited, which proved to be a significant success. This is because savings banks in Australia had been witnessing faster deposits than trading banks because the states guaranteed the deposits. Establishing a savings bank helped ANZ secure substantial deposits and regain some stability.

Domestic Operations Expand

In the early 1960s, as ANZ Bank's administrative hierarchy became more efficient, the ANZ decided to increase the bank's domestic operations as a strategy to increase earnings. There was a rapid expansion of branch banking operations. In six years, ANZ Bank opened 127 branches, 112 of which were in central business districts where the constituent banks of ANZ had always been under-represented.

Product Innovation

Despite the unfavorable regulatory environment and organizational issues, banks in Australia innovated products in the 1950s and 1960s. While other banks like ES&A diversified into selling hire purchase in the early 1950s, ANZ was much slower to enter this area.

An offer to buy an equity stake in one of Australia's leading hire purchase enterprises was turned down by ANZ in 1954 due to the differences of opinion within the organization about the best mode to get into the new business.

Eventually, it was only an announcement in 1957 by the Bank of New South Wales that it was taking a substantial shareholding in a hire purchase company that ended ANZ's indecision, and it acquired 14% of the shares of the Industrial Acceptance Holdings, which were retained until the merger with ES&A in 1970.

Venturing Overseas

Soon after building its first representative office in New York in December 1968, ANZ built its first office in Japan in 1969, making it the first ANZ outpost in Asia. However, it was only a modest existence for the first decade and a half before a proper banking license was granted to ANZ. Economic ties between Australia and Japan were growing, and much of the activity of the representative office was focused on strengthening those ties.

The Tokyo office opened just a decade after the 1957 Commerce Agreement between Japan and Australia, which was a remarkable achievement given the fact that World War II was still fresh in people's minds. In the 1960s, Japan was still rapidly modernizing, and by 1961, big Japanese commercial enterprises had established themselves in Australia.

Restrictions on foreign direct investment and capital controls were gradually relaxed after Japan joined the OECD in 1964, resulting in a flood of foreign banks opening operations around the same time. ANZ proved to be a key player in developing Australia-Japan trade and investment during the 1960s and became one of Japan’s most important trading partners.

The Merger Of ANZ and ES&A

Since 1955, ANZ Bank had been persuading the English, Scottish, and Australian bank for a merger. The board of ANZ Bank was impressed by ES&A's conservative lending and liquidity controls, its highly profitable hire-purchase subsidiary, Esanda, and its profit-oriented administration.

Moreover, ES&A also hailed from the same private trade banking tradition as the ANZ. Most importantly, the board of directors of ANZ believed that a larger bank would be able to command more resources than any of the banks could raise on their own.

Furthermore, some speculated that foreign banks would move in on ANZ's corporate and foreign operations, perhaps through ES&A as a host for entry. Eventually, the merger finally took place in October 1970.

The resulting Australia and New Zealand Banking Group Limited grew to be the commonwealth's third-largest bank, double the size of the fourth largest. Unfortunately, despite its increased market position, ANZ's profits declined, and spending increased during its initial years, owing primarily to sloppy administration and unexpectedly high merger costs.

Consequently, in 1973, the board hired a U.S. management consulting firm to help its executives revamp the ANZ Banking Group's organizational structure, frustrated by the deteriorating situation.

Finally, a modern defined planning system with long- and short-term goals arose, resulting in a more productive and efficient environment. Simultaneously, the consultants replaced traditional profit targets with targets based on return on assets.

The company's executives believed that this transformation would necessitate a substantial amount of capital. So, the board concluded that changing the bank's domicile would be in the bank's best interests. Hence, in February of 1976, ANZ's headquarters were relocated from London to Melbourne after 141 years. Two years later, the bank moved into the freshly completed ANZ Tower, a symbol of the firm's total metamorphosis in structure, philosophy, and character.

.avif)

Deregulation And Further Moves By ANZ

Since the Campbell Inquiry (Committee of Inquiry 1981) and the Martin Group report (Review Group 1984), the Australian finance sector and its constituent firms had been in an officially sanctioned state of flux. It was an ongoing debate that Australia could only continue to promote the capital flows required to develop its resource base if it joins the international game.

As a result, the previously restrictive Australian government policy started favoring progressive deregulation in response to the rising internationalization of the global financial system. Thus, the Australian banking sector had to mature quickly to compete on an equal footing with highly competitive international banks.

The perceived necessity for larger size to meet competition from the imminent entry of more foreign banks into Australia also resulted in an unseemly hunt for takeover partners in 1981.

Keeping the situation in mind, ANZ decided to try to buy strength and diversity. It merged with the Bank of Adelaide in 1979. In 1981, it also discussed combining with the Commercial Banking Company of Sydney and later the Commercial Bank of Australia, but neither merger went through.

In 1984, ANZ acquired Grindlays, which had offices in 40 countries. ANZ’s hierarchical authority structure was replaced by a horizontal organization with more than 50 business units worldwide.

These stand-alone businesses brought with them a creative and ambitious entrepreneurial attitude, as well as increased earnings. Although the bank's 1980s acquisitions, such as the purchase of New Zealand's PostBank in 1989, made ANZ the country's largest banking group and a major international financial player, it remained primarily a regional organization. In 1989, 77% of the bank's profits came from operations in Australia and New Zealand.

Key Takeaway 2: Explore Different Options – Always!

ANZ’s utilized multiple strategies simultaneously to survive and thrive in the second half of the twentieth century including opening a subsidiary savings bank, diversifying its product and service portfolio, expanding into new markets overseas, and following a policy of both international and local mergers and acquisitions.

All of these initiatives bode well for the bank as it continued to grow in size and stature both within Australia and internationally. ANZ’s route to success was paved by a set of consistent rules, the ability to adapt to changing times, and the willingness to persevere in the face of adversity.

From Rocky Times in the 1990s to Today's ANZ

Heading into the 90s, the ANZ Bank planned to continue its strategy of expansion through mergers. However, it didn’t prove to be very successful.

Facing The Storm

In 1989, ANZ and National Australia Bank, one of Australia's Big Four banks, began serious talks about merging. However, the merger was stopped by the Labor government, which was concerned about Australians' growing concerns about the dominance of the big banks in the run-up to a general election in March 1990.

After the unsuccessful merger of 1989, ANZ struggled to survive the harsh economic environment of the early 1990s, which featured high unemployment (peaking at 11%), high inflation, and high-interest rates in Australia.

The stagnation resulted in a surge in nonperforming loans, prompting ANZ and other Australian banks to set aside significant amounts of money to cover bad debts. The company's lowest point was in the year ending September 1992, when provisions of A$1.9 billion (US$1.3 billion) resulted in a net loss of A$579 million (US$399.3 million).

Eventually, as the economy improved and ANZ regained profitability, the bank resumed its international development, focusing mainly on East Asia.

Building A Holistic Strategy For Asia

In 1993, the business established a presence in Indonesia by obtaining an 85% stake in a joint venture bank, which was eventually renamed PT ANZ Panin Bank. In the same year, ANZ became the first English-speaking bank to open a branch in Hanoi.

Similarly, the bank entered China by opening offices in Beijing and Guangzhou, as well as a branch in Shanghai. By 1994, ANZ had become the largest foreign bank in South Asia, with its Asia-Pacific network accounting for 10% of the bank's overall revenues.

Even though the critics highlighted that many Asian countries face sovereign and regulatory risk, combined with the possibility of lower shareholder returns, ANZ decided to venture into various Asian countries in order to diversify its operations.

ANZ.Com Goes Live

In 1996, ANZ aimed to move clients to more convenient and efficient electronic delivery channels to achieve internal efficiency benefits. The greater use of electronic channels aided the reconfiguration of ANZ's distribution network, and the number of branches was also lowered from 320 to 259. Alternative specialist sales channels, such as mobile mortgage managers, were also being tested or extended simultaneously.

Moreover, telephone banking had witnessed a significant increase in registered customers, resulting in market penetration of roughly 10% of the population. ANZ also developed new products to deliver banking services electronically, such as ANZ.com, a website that launched in 1996 and was quickly followed by the then-revolutionary phone and internet banking channels.

The Asian Currency Crisis Hits

In mid-1997, Asia experienced one of the largest exchange rate drops. From 1992 to 1997, the region's economy grew at a 7% annual rate, but it was expected to drop in the coming years significantly due to the currency crisis.

As the region continued to be plagued by high levels of bad debt, nonperforming loans peaked in Asian countries. Inevitably, the Asian turmoil also harmed ANZ because of its longstanding international franchise.

Early in 1998, the bank formed a specialist team to deal with the situation and minimize its exposures. As a result, the group was able to provide targeted management of the situation. The year's specific provisions were kept at $512 million, with $263 million allocated to Asia.

Keeping in mind the situation, ANZ also significantly reduced non-strategic assets in Asia. Furthermore, lending policies had been reviewed and tightened to place a greater emphasis on network business, particularly trade finance, rather than foreign currency lending to local firms.

Furthermore, through its trading activities in London, ANZ was exposed to the collapse in emerging market bond prices, resulting in losses of $83 million on trading securities (compared to a profit of $182 million in 1997). Nevertheless, in 1998, ANZ boasted a profit largely similar to that of the previous year.

It achieved record results in Australia and New Zealand, which were up 16% and 28%, respectively, to offset a decline of 39% internationally. This was a big accomplishment in a challenging environment, and it highlighted ANZ’s domestic businesses' transition over the last two years, as well as the group's diversity.

21st Century Changes

In April of 2000, ANZ announced the sale of Grindlays to Standard Chartered Bank. On July 31, the sale was finalized, with ANZ obtaining $2.3 billion in total consideration, including a $1.2 billion premium above book value.

The sale of Grindlays allowed ANZ to "simplify and focus" its international network in one stroke, marking a significant step forward in the company's ambition to recast itself as a more balanced organization.

Then, in May 2002, the first major joint venture agreement based on the new growth formula was signed. With A$38.4 billion in funds under management and becoming Australia's number five life insurer, ING Australia quickly rose to fourth place. The main point behind the deal was that it would combine ING's fund’s management expertise with ANZ's bank distribution channels.

This was a significant development for ANZ, as it addressed a strategic void in wealth management. In the early 2000s, one of the fastest expanding areas of financial services was wealth management.

Wealth protection, as well as the need to fund one's retirement, were becoming increasingly important to Australians and New Zealanders.

In 2003, ANZ purchased The National Bank of New Zealand, making it the largest bank in New Zealand and the clear third largest bank in Australia by market capitalization.

ANZ did so while providing a robust 17% total shareholder return for the year, far exceeding the sector average. It was a unique acquisition in that it was built on combining the assets of both firms to improve customer service, satisfaction, and growth.

In Asia, ANZ completed the acquisition of companies in 2010 from the Royal Bank of Scotland in six countries as part of its super regional strategy. Together, the businesses formed an appealing portfolio of well-provisioned banking assets at a reasonable price that complemented ANZ's existing operations.

ANZ has also been one of the most forward-thinking financial firms, particularly in the areas of green and social impact finance. The bank signed the first arrangement with Fortescue Metals in 2018 as part of a $50 million funding program to assist Aboriginal firms in obtaining equipment financing.

Not only that, but ANZ also pledged to aid Australia's economic recovery and transition from the Covid-19 outbreak by launching a support package for small business and home loan customers.

Key Takeaway 3: Adapt According To The Situation

ANZ never stopped looking for new ways to expand and maximize its shareholder value. It continued to grow by making a slew of large and small acquisitions and creating strategic alliances with domestic and international businesses. Not only that, ANZ continued to support and promote sustainability and innovation.

Digital Transformation Need of the Hour for ANZ

In recent years, ANZ has refined its business strategy through its ambitious plans to adapt to the rapidly evolving market and people’s changing needs and preferences for digital products and services. The bank is going the extra mile to keep pace with digital innovation and offer its customers reliable and high-quality experiences by harnessing the power of technology.

Right from 2010 when ANZ launched its GoMoney smartphone app - Australia's first ‘mobile to mobile’ or 'person to person’ payment app - and becoming the first major Australian bank to offer consumers a new option to make contactless payments via Apple Pay in 2016 to today where the bank is doubling down on digital transformation, ANZ has been one of the few conventional banks trying it best to digitize.

But the main question is whether it's enough to combat the threat posed by neo banks and digital banks. Can ANZ survive, let alone prosper, in a world that is fast evolving and embracing new technologies?

Competition Is Heating Up

Increased competition from digitally-enabled competitors is a key risk to ANZ. The bank is under significant pressure from new financial services entrants such as neo banks and digital banks, which are transforming banking and delighting customers to the point that they have no choice but to switch banks.

Douugh and archa were established in 2016, Xinja, Up, Volt, and Judo debuted in 2017, and 86 400, Hay, Pelikin, Qpay launched in 2018 - these are 10 neobanks and digital banks that have had a headstart over ANZ, which has been extremely slow to digitize and harness the power of technology.

Despite their infancy in Australia, neobanks and digital banks are making a name for themselves. In May 2020, Judo raised $230 million, bringing its total cash raised to $750 million. Xinja announced that $30 million was deposited in the first seven days of operation, with more than half of those customers originating from the Big Four. Hard to believe, isn’t it?

Furthermore, 86 400 recently reported that a year after receiving its APRA banking license, it has over 225,000 accounts, has received over $300 million in customer deposits, and has processed over $1 billion in transactions. No wonder National Australia Bank Limited (NAB) acquired 86 400 and other banks, such as Bendigo and Adelaide Bank is all set to acquire fintech Feroicia in a bid to gain control of the digital bank, Up.

There’s no doubt that digital banks and neobanks are revolutionizing the banking industry, in an effort to keep up rather than understanding, addressing, and adapting to the changing financial landscape, banks are acquiring neobanks and digital banking technology.

The fact of the matter is that ANZ has no alternative but to transform digitally and offer more tools, support, insights, and resources to serve its customers.

Threats From Cyberattacks Increasing

ANZ realizes that increased cyber-attacks, scams, and attempted frauds can threaten its very existence.

Cybercrime and digital fraud have the greatest impact on financial businesses. According to the most recent data from the Australian Cyber Security Centre, self-reported cybercrime damages totaled more than $33 billion in 2020. From 2020 till 2021, the Centre received 67,500 reports of cyberattacks, which is the equivalent of one attack every eight minutes.

Let this sink in. The most common types of cybercrime recorded were fraud, online shopping scams, and online banking scams. Clearly, banks are falling behind in combating today's sophisticated cyber-attacks and digital scams. This is primarily due to a lack of investment in digital transformation and the enhancement of existing systems.

Like the majority of other banks, ANZ has not put in place adequate procedures to detect, monitor, and eradicate cyber-security threats. Mark Whelan, ANZ's head of institutional banking, claimed the number of attacks had increased during the pandemic to the point where the bank was receiving 8 to 10 million attacks every month.

This puts the customers at a huge risk. ANZ has been criticized on several instances, including an attack on its online banking service and app in September 2021 when the ANZ banking services were shut down for at least three days due to a distributed denial of service (DDoS) assault that caused sporadic access to their websites.

Legacy Systems Bogging ANZ down

Legacy banking systems are conventional platforms that banks use to maintain their back-end infrastructure for fundamental activities like opening new accounts, processing transactions, receiving deposits, and initiating loans, among other things.

They generally refer to inefficient systems that are unable to cater to the growing demands of today and tomorrow. On top of this, they are expensive to maintain and operate.

These legacy banking systems are frequently referred to as the most significant challenge confronting banks looking to grow and go digital. These outdated systems are simply not capable of meeting the expectations of today's consumers, and they expose the bank to additional risks and liabilities.

For example, ANZ's core system was down for hours in October 2021, leaving clients without access to online banking, causing losses for both the customers and the bank.

Every day, the gap between neobanks and traditional banks continues to widen and legacy banking systems only pile on the pain for banks, bogging them down. For example, even something as simple as creating a bank account is made slower by the banks’ legacy systems and processes.

On the other hand, digital/neobanks can open accounts in seconds, and that too digitally. ANZ is trapped in the past, clinging to inefficient and rigid legacy systems that are ineffective and inflexible when it comes to meeting today's demands and planning for the future.

While digital banks and neobanks are offering innovative digital products, harnessing the power of data and analytics, providing a human-centered design and impeccable online customer experience.

Lack Of Digital Offerings

According to PWC’s 2021 Digital Banking Consumer Survey, more consumers than ever banked digitally with 61% of consumers interacting weekly on digital channels and 20-25% of people preferring to open an account digitally but are unable to do so.

The truth is that digital experiences and platforms are no longer optional; instead, customers expect and prefer them. According to McKinsey & Company, 75% of consumers who used digital channels for the first time in 2020 said they would continue to use them once things returned to "normal."

Clearly, digital banking is here to stay as the rapid migration to digital technologies during Covid-19 will become permanent as we move forwards.

Though ANZ has taken some measures to make fintech a bigger part of its organization, there's still a lot more work to be done given where things are currently.

ANZ is lagging behind in providing quality digital offerings that are simple and convenient to use, from point-of-sale financing and buy now, pay later solutions to advanced analytics and personalized loan and payment services. As a result, existing clients will have no option but to change who they bank with.

Key Takeaway 4: The Future of Banking Is Digital

It's about time ANZ steps up its game. After all, it possesses the necessary capital, resources, and experience to negate neobanks and digital banks. The key difficulties holding ANZ back are its lack of digital culture, inefficient legacy systems, sophisticated cyber threats threatening its very existence, and difficulty in providing innovative digital solutions.

With rapid technological breakthroughs and digital becoming widespread, ANZ must take action and develop a digital-first corporate strategy that is able to meet its customers’ needs.

Growth By Numbers & Key Strategic Takeaways

ANZ’s growth over its journey of close to two centuries has been truly spectacular with many ups and downs. Today, ANZ is undergoing a transformation to stay relevant and survive as well as thrive. All this while, it is continuing to do what it does best: empower people and communities by improving financial well-being and sustainability.

It is doing that by focusing on helping people save for, buy, and own a home; start and grow their business, and enabling companies to move goods and capital effectively.

Growth By Numbers

Always Have A Specific Vision

Right from the very beginning when the Union Bank of Australia and the Bank of Australasia stood out due to their laser-sharp focus to tackle the various challenges, ranging from depressions, wars, floods, and fires to stand tall and continue to grow to today, ANZ bank has continued to operate with a specific vision. ANZ bank today, unlike other banks, has a particular purpose and vision.

It aims to shape a world where people and communities thrive by enhancing the financial well-being of customers, enabling them to own a house, start or grow their business, and help companies move around goods and capital. Such a precise vision allows ANZ to craft a strategic plan, build an amazing organizational culture, motivate employees, and pursue its purpose with clarity and confidence.

Embrace New Opportunities

ANZ started with the merger of the Bank of Australasia with the Union Bank of Australia in 1951 to form today’s ANZ Bank. Ever since, it has been involved in a number of acquisitions and mergers. In a competitive interatrial market to obtain a competitive advantage and scale-up, multiple growth options must be explored.

Mergers provide a lot of advantages, ranging from boosting market share and lowering operating costs through economies of scale to the diversification of risk. It's no surprise that ANZ used them to expand globally.

Avoid Complacency

In today's business environment, change is unavoidable. Knowing how to successfully navigate these changes and develop appropriate and effective processes to adapt is a must. The key to ANZ’s success is the fact that it has always looked for opportunities to improve, taken risks, innovated, and tried new approaches to figure out what works and what doesn't. It’s essential for businesses to venture into new areas, explore new options, and take whatever good opportunity comes their way.

ANZ has been able to consistently raise the standard, delight its clients, and fuel its growth as a result of its proactiveness. By remaining watchful of the situation and never becoming too complacent even in good times, ANZ has always managed to navigate relatively smoothly from tough times, a prime example of which is the Australian banking crisis of 1893.

Stand Firmly In The Face Of Adversity

ANZ has always focused on operational excellence and displayed remarkable resilience to support its long-term growth. ANZ’S business model, strategy, governance, and risk management processes are well thought-out and help it evaluate risks and opportunities in its operating environment and deliver value for its stakeholders. From World War I to the Asian currency crisis to the Covid-19 pandemic, ANZ has always remained adaptable and agile in response to what may come next. It is this flexibility and proactiveness that make ANZ truly shine.