Headquartered in Perth, Western Australia, Bankwest functions as a division of The Commonwealth Bank of Australia (CBA), the biggest Australian bank and the largest Australian company listed on the Australian Securities Exchange.

Bankwest occupies a central position as a leading financial services institution in Australia. So much so that it's impossible not to bring up Bankwest when considering Australia’s finest banking and financial services institutions.

Bankwest offers a diverse range of banking and financial services, specifically: Personal Banking, Business Banking, Commercial Banking, Corporate and Private Banking, Trade Finance, Agri-Business Finance, Credit Cards, and more.

Not only is Bankwest committed to providing the best financial solutions, but it is also endeavoring to make the whole experience simple, friendly, and safe. Its dedication to simplicity and transparency has been the driving force behind its success over the years as it grew both in numbers and as an institution as a whole.

Here are some facts and figures to illustrate its current status:

- More than 3000 employees serving customers all over Australia

- Boasts an illustrious history of 125+ years

- First non-major bank to win MPA Magazine Brokers on Banks, Bank of the Year 2020

- Has a Consumer NPS (Net Promoter Score) of 11.8

- Has a Business NPS (Net Promoter Score) of 23.8

Bankwest has come a long way since it was established in 1895. Over the course of its journey spanning over 125 years, Bankwest has strived to put customers at the heart of its business.

Let’s take a closer look at how it has managed to evolve over time.

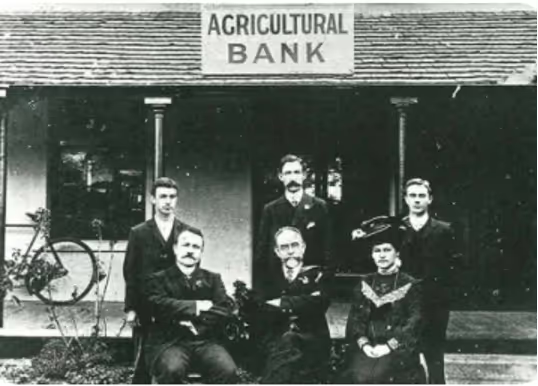

From the Agricultural Bank of Western Australia to Bankwest

Bankwest has followed a fascinating developmental trajectory. It started off as a mere State-owned bank for the facilitation of farmers and the promotion of the Agricultural Industry of Australia, ultimately branching itself out as a banking and financial services provider by the 1900s.

Bankwest’s Agricultural Origins

On the 23rd of November, 1894, the Government of Western Australia set up the “Agricultural Bank of Australia” to assist the country's weak agricultural industry and farming situation. It was the original institution that would eventually become the Bankwest we know of today.

The aim was to enhance and improve the sector as much as possible and boost it by increasing occupation and agronomy practices.

As the bank was established to aid the public, it took no deposits from them. It only gave farmers loans amounting to 300 pounds on as little as 1% interest. This deal was offered in exchange for successful agricultural restoration practices, like cultivation, draining or clearing of land, vine or orchard sowing or fencing, and ring barking, among others.

At this point, the bank's sole purpose was to facilitate restorative agricultural practices and support the industry by offering financial services to farmers.

Incentivizing The Industry

In 1906, the government increased the loan amount to 400 pounds, with the capital also doubling. The bank maintained these rates till 1912 with very few revisions in the government’s policy.

The goal of this policy was clear: it was to allow the Australian Government to strengthen their agricultural industries by offering achievable incentives to farmers while losing out on no unnecessary funding with the markup rate at 1%. In fact, it was actually able to make a small profit instead!

From 1914 to 1916, Australia suffered droughts which led to decreased loan returns and repayments. However, the bank continued to give out loans to as many people who came to avail themselves of the opportunity and helped support the farming industry in trying times.

More Than A Name Change

In 1916, the bank’s name was changed from “Agricultural Bank of Australia” to the “Rural and Industries Bank of Western Australia.” The name change was prompted by the passing of the Rural & Industries Bank of Western Australia Act 1916.

{kind=link}

The Act essentially transformed the bank from a small mortgage bank to a larger, State-Owned Trading Bank. Consequently, the interest rate was increased to 6% on every loan taken, and an Industry Assistance Board was established to further help the farmers who had already settled on the land.

In 1917, loan repayments were set at a maximum of 5 years, and the first 20% of the unpaid amount was to be recovered by the Board, while the rest went to other shareholders.

Taking On A Bigger Role

In 1945, due to the improved Rural and Industries Bank Act Of 1944, the R&I Bank of Western Australia became a highly involved benefactor to help out in various government schemes.

Its functions grew to include assisting in the budgeting and allotment of monetary assets to the State of Australia, such as the Commonwealth Reestablishment Scheme (CRE), War Service Land Settlement (WSLS), Dairy Farm Consolidation Plan (DFCP), and Farm Management Advisory Service (FMAS), among others.

These developments contributed to the bank’s expansion and paved its way for becoming a commercial bank.

Further on, in 1956, it also became a Savings Bank. In 1985, it opened its first official branch in Sydney, which provided greater opportunities for growth and retail diversification in the market.

Becoming Bankwest

The R&I Bank of Western Australia enjoyed remarkable evolution and growth in the latter half of the 20th century.

In 1990, it officially acquired an incorporation title accompanied by a name change - the bank was henceforth to be known as the “Bank of Western Australia Limited” while trading under the name “BankWest.” The change was implemented for the sake of privatization as well.

{kind=link}

Bankwest could now deal with Home Loans, Term Deposits, and Credit Card services, among others - successfully transitioning into a fully integrated commercial bank.

Bank Of Scotland Acquires Bankwest

Then, in 1995, the Bank of Scotland bought out Bankwest - which at that point was Australia’s largest Home Lender, State-Owned Bank. Thus after a purchase amounting to A$900 million, the Bank of Scotland became Bankwest’s parent company.

The Bank of Scotland offered 49% of Bankwest’s shares to the public for investment as part of the sale agreement. This move was partly due to the uncharacteristically large numbers of debts collected and losses suffered by the Government in the 1980s.

Finally, the shares offered were displayed on the Australian Stock Exchange on the 1st of February, 1996. Bankwest underwent complete individual privatization on March 1, 1996.

Key Takeaway 1: Change Is Essential For Growth

The key to Bankwest’s growth is that it was able to transform over the years to become the Bankwest of today. The various stages of the bank’s evolutionary process increased its capacity and broadened its functions.

When it became Bank of Western Australia, it expanded the range of services it offered and transitioned into a commercial bank.

Although the changes plunged the bank into unknown territory (in a new role and capacity), it continued to flourish as it took on additional functions and began offering a diverse range of financial solutions.

Acquisitions Pave The Way For Further Growth

The new millennium saw Bankwest go through further developments until it eventually got acquired by the Commonwealth Bank of Australia and became a leading financial services brand.

Speculating About The Future Of Bankwest

In 2001, the Bank of Scotland had merged with Halifax to form the HBOS group. In 2003, HBOS was looking to acquire the remaining 43% of Bankwest stakes.

Speculations were rife as to the implications of such a move; some considered it to be a telling sign that HBOS meant to dispose of the entire operation. However, a spokesperson from HBOS clarified that the organization simply sought to maximize the value of its existing investment.

The top management of HBOS considered Bankwest to be a worthwhile investment but to maximize its potential; it required a level of support and commitment from HBOS that the latter was not willing to lend as a partial owner.

Therefore, HBOS needed to acquire the remaining shares of Bankwest for it to realize its full potential. Consequently, Bankwest soon became HBOS’s wholly-owned subsidiary.

Bankwest’s Industry Specialization Growth Strategy

In 2003, Bankwest acquired the finance subsidiary of Australian Pharmaceutical Industries (API) as the pharmaceutical wholesaler had decided to focus on its core business.

Through the acquisition, Bankwest became the preferred supplier of loans and other financial products and services to API pharmacy customers - including a network of pharmacists around the country.

The acquisition was significant as API Finance’s client base primarily consisted of individuals with high net worth and had a low probability of default. Bankwest’s expansion into the healthcare sector is part of a larger plan to identify and capitalize on avenues of growth.

The acquisition was also expected to yield a revenue uplift for Bankwest in 2003 and the potential for growth in subsequent years.

Uncertainty Strikes Once Again

In August 2008, HBOS indicated that it would be interested in cutting down its non-core businesses. However, HBOS’s chief executive did emphasize that Bankwest’s sale was not forced as it had reported strong capital ratios and raised $7 billion in its recent rights issue.

However, HBOS was prompted to divest parts of its businesses to improve its capital ratios further and reduce its wholesale funding requirement. It was a tempting prospect, given the constrained market conditions at the time.

The Commonwealth Bank of Australia emerged as the most likely buyer of Bankwest. It had forgone the opportunity to acquire the Royal Bank of Scotland in favor of Bankwest.

The most attractive feature about acquiring Bankwest was that it could enhance CBA’s position in the retail market - specifically the home loan market.

CBA Buys Bankwest

In October 2008, the Commonwealth Bank of Australia officially agreed to buy Bankwest from HBOS along with other assets for A$2.1 billion. The purchase of Bankwest proved to be quite economical for CBA as it was 20% below book value.

HBOS was adversely affected by the global credit crisis, and its shares had slid considerably, thus prompting a broad-based sell-off.

The acquisition of Bankwest was expected to bring various benefits to CBA, such as a boost in its market share in Western Australia - a region undergoing rapid growth.

Moreover, the acquisition was expected to boost CBA’s earnings per share immediately. The combination of Bankwest with CBA would create a formidable group.

At the time of its acquisition, Bankwest had 860,000 customers - with a vast majority of them being in Western Australia, which was experiencing rapid growth due to the boom in mining operations.

Bankwest had also been branching out its retail banking operations in populous markets of Eastern Australia.

All in all, Bankwest provided an interesting opportunity for CBA to invest in, and the decision has proved to be a good one as Bankwest is now one of its thriving subsidiaries.

Key Takeaway 2: Weather The Storm Come What May

The years since 2000 proved to be an uncertain time for Bankwest as it was involved in numerous speculations concerning its acquisition.

However, Bankwest was always an asset instead of a liability for its parent company. Even while speculations concerning its potential disposal were spreading, it was apparent that the reason for selling it was not because of its poor performance.

Bankwest essentially weathered the storm because of its solid business grounding and the fact that it had created a brand value for itself.

The Bankwest of Today

The Bankwest of today is completely transformed from when CBA acquired it and functions as a successful brand under CBA’s umbrella.

Bankwest, now more than ever, is committed to delivering a simple, friendly, and safe banking experience for everyone and enhancing the financial wellbeing of all. It does so by reducing the amount of “bank” in people’s lives without any gimmicks whatsoever - i.e., making the processes so convenient that the need to go to a bank physically becomes obsolete.

Beyond Just Business

Bankwest is not just focused on delivering superior financial products and services but is also working towards creating a positive impact on its communities.

BANKWEST CURTIN ECONOMICS CENTER (BCEC)

Bankwest also supports research into issues affecting Australian families, communities, and businesses. The BCEC produces high-quality, accessible research that aims to influence economic and social policy nationwide. Right from 2012 to today, Bankwest continues to offer support to BCEC.

VOLUNTEERING

Bankwest has a number of partnerships with various welfare organizations and charity groups that provide opportunities for employees and the community to get involved.

Bankwest offers its employees two days of paid leave a year to volunteer at charities and community groups. On average, Bankwest’s over 3000 employees do 7000 hours of volunteering each year.

BEACON APP

Bankwest partnered with Telethon Kids Institute in 2020 to deliver the first Australian cyber safety app - “Beacon.” It helps parents keep their children safe by providing them with the latest info about risks and threats such as online grooming, cyberbullying, and stalking.

Moreover, it can also create customized family agreements to encourage and enable healthy online behaviors, expectations, and boundaries.

It took three years to combine 14 years of cyber behavior research at Telethon Kids Institute and Bankwest’s digital and cyber safety expertise to help make the app a reality and bring about a positive contribution to children’s online safety.

Equality & Inclusion - A Bankwest Priority

Bankwest strives to grant equal access to opportunities to all so that it can realize its potential.

It provides its workers with a safe environment where they can bring their whole self to work, creating a vibrant and inclusive culture. The efforts all culminate under the “Inclusion at Bankwest” strategy.

Several networks have spawned because of this strategy.

- UNITY - the LGBTQIA+ and allies network that advocates for a culture of inclusion and respect, regardless of sex, sexuality, gender, or expression

- MOSAIC - celebrates cultural diversity and fosters inclusion and respect

- KOORT WAANGKINY - gives a voice to Aboriginal and Torres Strait Islander peoples, and those passionate about supporting Bankwest’s reconciliation initiatives within the business

- ADVANTAGE - is focused on creating a diverse and inclusive workplace, where people feel valued, respected, and are able to perform at their best

- ENABLE - is increasing accessibility awareness, inclusion, and employment opportunities for people with disabilities

Playing Its Part

Bankwest is dedicated to advancing reconciliation in Australia, with its locations spanning 29 Aboriginal people’s lands and 11 nations.

Bankwest’s Reconciliation Action Plan was devised to try to improve the financial conditions of the Aboriginal and Torres Strait Islanders customers and communities.

In addition to this, Bankwest actively supports Reconciliation WA programs and initiatives. Moreover, it has initiated cultural awareness training and introduced eLearning opportunities for employees.

It has even set up the Customer Assistance Line to tend to specific needs of the Aboriginal and Torres Strait Islanders customers.

Bankwest Through Covid 19

The peculiar circumstances created by the pandemic prompted Bankwest to introduce various schemes to help people through financial hardships. From individuals to businesses, Bankwest helped everyone in its capacity to cope with unprecedented challenges.

The bank also continues to support its customers through an assistance mechanism - Customer Assist Team. The Customer Assist Team helps and guides the customer through ways they can manage their credit cards or loan repayments if they are unable to meet their monthly repayments or require financial assistance.

Key Takeaway 3: Doing Good Business Means Doing Good

Bankwest has developed an extensive support system that goes beyond the avenues of regular business. It indicates Bankwest’s standing as a socially responsible organization.

However, all these efforts towards caring for the community and doing good ultimately translate into good business. Caring for employees and communities goes a long way to ensuring a healthy and productive working environment, which is critical for growth and success.

Moreover, an organization’s efforts towards social responsibility also get recognized by customers and clients, which helps form a reliable and sincere business network.

Key To Further Success: Digitization!

Over the years, Bankwest has realized the importance of evolving its business strategy and diversifying its products and services through digitization.

The introduction of new digital products and services is an area of focus that is key to revitalizing the business and breathing new life into the brand.

The emphasis on digitization is part of the company’s customer-centric innovation strategy.

Changing Market Dynamics

Recent years have seen a surge in new entrants in the market. These new financial services providers are luring customers away from traditional banks with the promise of a much more convenient and frictionless digital experience.

Bankwest and other established banking institutions face pressure from these neo banks and digital institutions to undergo a digital transformation. Moreover, customer expectations of their financial service provider are also rapidly evolving.

In order to stay relevant and maintain its customer base, Bankwest has no choice but to reorient itself in a way that is best suited for future success.

Within the new context, digital transformation is the deciding factor for Bankwest’s survival in an increasingly digital environment.

Facing A New Type Of Competition

In the 2018 presentation at the CIO Summit in Perth, Bankwest’s head of technology, Andy Weir, pointed out Tyro as a relatively new player in the market (14 years as opposed to Bankwest’s 125) that successfully processed more than $9 billion in payments and has even secured a banking license.

Weir also explained how the competition faced by Bankwest from these new financial service providers is fundamentally different. These new players are not bogged down by legacy challenges that established banks like Bankwest are.

Instead of just being a technology issue, the challenge for Bankwest is more about pursuing a more ambitious customer-centric strategy.

Customers are increasingly looking for more convenient and frictionless service, and traditional banks are lagging behind neo banks and digital financial service providers in that arena.

How Bankwest Has Responded To The Challenges

Bankwest drew inspiration from its parent company, the Commonwealth Bank of Australia (CBA), for its digital transformation. CBA had initiated its own modernization project in recent years that was geared towards developing more customer-centric retail and commercial services.

CBA had managed to raise its profitability, lower costs, and create a more engaging client experience. Bankwest sought to replicate CBA’s success by undertaking an extensive digital transformation of its own.

Following are the significant steps that Bankwest has taken to ensure its survival in the digital arena and to enhance its customer experience:

“Bank less” with Bankwest - Agile Transformation

Recognizing the need for meeting the challenges of the industry head-on, Bankwest initiated its “Agile transformation.”

Taking 1000 staff members from across the business and IT departments, Bankwest mobilized them into cross-functional, multi-disciplinary squads aligned with customer tribes.

Doing so has enhanced the efficiency of a traditional procurement and development cycle, allowing Bankwest to adapt to changes rapidly. Agile is an approach located within a larger business strategy that aims to incorporate a customer insight, data-driven model.

The strategy’s main emphasis is on promoting a customer-centric culture within the business. Bankwest's strategy has resulted in rapid innovation via digitization.

The Bankwest App

The Bankwest App is geared towards making banking secure and convenient for its users.

Its most popular features include:

A 24/7 in-app messaging service that offers real-time support to its users via their phones. The feature was a first for Australian banking that worked across devices and platforms.

Ease of using digital cards to make payments on the go without having to carry a physical card with you. The app also allows users to safely and securely copy their card details when shopping online - saving them the hassle of manually typing in the details every time.

Keep track of users’ transactions and see who’s really charging them. The app provides detailed info about the business type, location, and contact info - putting an end to transaction mysteries and offering peace of mind to its customers.

An Easy Alerts notification system that allows users to keep updated on important activities on their accounts. The basic alerts include payment notifications, credit card repayment reminders, and an alert that notifies users when their account has dropped below a set amount.

The Bankwest app also includes a range of payment options such as cardless payments, paying to another account, PayID, sharing payment receipts.

Users can even personalize their banking experience through certain features on the app, such as setting up their own savings goals, nicknaming and reordering their accounts, and bucketing their money by setting up different accounts for different expenses.

Bankwest Makes It Easier For SMEs to Raise Credit

Bankwest identified the need to provide a faster application process to SME customers that wanted to raise credit. Decision-makers at SMEs seek to avoid drawn-out application and verification processes.

Thus, Bankwest invested in developing a top-notch onboarding process that simplifies and accelerates access to capital for SMEs. The initiative even earned Bankwest the “Best Omni-Channel” and “Best Digital Platform” at the 2017 Australian Business Banking Awards.

Bankwest Launches End-to-End Digital Homebuying

Because of the COVID-19 Pandemic, social distancing restrictions prompted Bankwest to develop a faster and more convenient home buying experience.

In April 2020, Bankwest launched an electronic identification (eID) process for new home loan applications, enabling brokers to remotely verify the customers’ identities.

The eID coupled with Bankwest’s digital signing has formed an end-to-end digital homebuying experience. With the digital signing feature, the processing time of new home loan applications has been reduced by two weeks. Moreover, it offers faster proofing/error-checking and a more robust digital audit trail.

Looking At The Bigger Picture

Despite the positive steps taken towards digitization, the challenges faced by Bankwest are still too great. In order to catch up with the neo banks and digital banks that have had a head start on Bankwest.

The four key challenges faced by Bankwest in its quest for digital transformation are as follows:

Ensuring Safe & Secure Banking

A common challenge across the whole banking industry is the significant risk of cybercrime and digital fraud. According to some estimates, cybercrimes cost $6 trillion globally in 2021, with banks being the worst affected.

Banks’ vulnerability to cyber-attacks and digital frauds results from a lack of internal digital transformation. While the threats and risks continue to evolve with the adoption of new technologies and digital solutions, banks are ill-equipped to face the enormous threat.

Although Bankwest has local experts trained in scam detection working around the clock and has various account and card security mechanisms in place, it is still insufficient compared to the threats it faces.

Legacy Systems Hinder Transformation

Legacy banking systems are outdated platforms that banks use to support their back-end infrastructure for essential services such as making new accounts, processing transactions, initializing loans, etc.

As such, these systems do not possess the capacity to cater to today’s customers’ needs efficiently. Moreover, legacy systems are costly to operate and maintain as well.

In 2006, Bankwest underwent a critical outage, with most of its systems being down for two days. A similar disaster occurred in 2016 when Bankwest lost most of its customer-facing systems for four and a half hours in the middle of the day.

In contrast, the newer financial service providers such as Tyro are not bogged down by legacy systems and have not suffered a system outage as Bankwest has.

Building Up A Culture Of Digitalization

Another significant challenge faced by traditional banks is that they are unable to adapt to changing market dynamics because of a lack of digital culture.

The organization lacks the motivation to acquire an edge by leveraging technology and digital tools from the get-go.

Although Bankwest has initiated efforts to inculcate a culture to promote internal digital transformation (Agile), it is a long process. One wonders how long a traditional bank needs to catch up to its new competitors that have the advantage of a head start and are not weighed down by old infrastructure and attitudes.

Any efforts for digital transformation must ensure that everyone from the top management to staff in the back offices and front lines shares the same vision. Such an extensive change to organizational culture would require time and consistent effort to achieve.

Ramping Up Digital Solutions

Financial technologies will soon drive out traditional banking systems and institutions from the market. If Bankwest fails to rise to the challenge, it might just be one of them.

Customers are increasingly turning towards fintech platforms, and Mckinsey & Company report that over 90% of them are satisfied with them.

Despite Bankwest rolling out its own range of digital financial solutions, it is still lagging in the race. There is a considerable need to do more and diversify its digital portfolio with innovative solutions to retain customers and attract new ones.

Introducing a customer-centric digital innovation model is a step in the right direction, but the destination is still a ways off.

Looking Towards The Future

Bankwest currently stands on the precipice of either a crucial breakthrough or ultimate failure to meet the needs of an evolving market. If it is successful in adopting digital technologies and can reorient itself as a financial technologies innovator, it can become a leader in the financial industry.

The challenge is enormous, but Bankwest has indicated its determination to rise to the challenge by introducing various strategies and digital products to intensify its digital rebirth.

Key Takeaway 4: Prioritizing Internal Digital Transformation

The only hindrance to Bankwest’s growth is the lack of internal digital transformation. The key factors keeping it from progressing further in the digitization process are outdated legacy systems, lack of a digitalization culture, lack of digital solutions, and insufficient security mechanisms.

Nevertheless, Bankwest has prioritized internal digital transformation and has adopted the Agile approach to create the latest fintech solutions and a culture of digitalization within the organization.

The launch of new features on the Bankwest app aims to attract not only customers but also brokers and SMEs.

Bankwest is determined to tackle the challenge of internal digital transformation. Only time will tell how successful its efforts will be.

Summary & Strategic Takeaways

Bankwest has achieved extraordinary success and growth over 125 years. It went from being a governmental institution meant to provide financial services to farmers to becoming one of Australia’s finest banking and financial services brands.

It has contributed to its community, giving back to society through volunteering, and strives to offer its clients the best user experience. It has created a legacy for itself that speaks of its strong guiding principles, clarity of vision, and capacity to adapt to change.

Although it is faced with increased pressure from new and emerging competitors, Bankwest continues to pave its way forward even amidst these challenges.

{kind=link}

Be More Than Just A Business Focused On Profits

Throughout the years, Bankwest has operated according to its core principles of care, courage, and commitment. It has strived to put customers and communities at the heart of its business.

It has pursued various community initiatives and encourages a culture of volunteering and support amongst its employees. Its customer assistance mechanisms have reached out to those afflicted with financial hardships during the pandemic.

By incorporating the principles of care and support into its business model, Bankwest extends a sense of more profound connection with its clients, communities, and employees.

This approach helps differentiate Bankwest from the competition and helps develop a loyal and happy customer base. The positive synergy created as a result of this approach feeds back into the business in the form of improved performance and strong internal support networks.

Adaptability Is Crucial For Survival

Within an ever-evolving market, where technology and customer expectations are rapidly changing, an organization’s capacity to adapt and transform becomes the key to its survival.

Bankwest has proved time and again that instead of cowering in the face of change, it rises to meet the expectations of its clients in innovative ways.

It has also demonstrated that it is not afraid of introducing drastic changes to its business model for the sake of staying relevant in the market. The Agile approach and efforts towards internal digital transformation are proof of the fact.

Moreover, Bankwest has also incorporated the principle of customer-centrism into the very fabric of its business model. All of its efforts towards digitization and the development of new products and services are guided by this vision.

Create Lasting Brand Value

Another thing that Bankwest’s journey has illustrated is the importance of creating brand value. During its time of uncertainty, when Bankwest was being acquired and sold off, it was always an asset to its parent company.

The value the brand had created by itself was what had attracted CBA to ultimately acquire it. Bankwest’s acquisition had resulted in positive developments for its parent company, so it became a valuable asset that could offer value of its own.

The development of brand value was a crucial factor for the continued growth and success of Bankwest as a brand.

By expanding its customer base and branching out to markets beyond Western Australia, Bankwest provided an enticing opportunity for any organization looking to acquire or reinforce its footholds in the region.

Growth And Change Go Hand In Hand

In the initial years of Bankwest’s growth (during the late 1800s and early 1900s), it constantly underwent critical changes. It adjusted its working model and incorporated a wider range of functions as it grew.

It went from being a state-owned entity to being publicly listed on the Australian Stock Exchange in 1996.

Even in recent years, Bankwest has been taking great pains to change its current business model to better adapt it according to customer needs and expectations. Transforming itself is the key to success and future growth.

Instead of being afraid to venture into new avenues of growth, Bankwest is increasing its capacity for further success.