Wells Fargo is an American multinational financial services company, streamlining financial access for millions of consumers and thousands of businesses in the US.

Wells Fargo’s market share and key statistics in 2021

- Total Revenue of $78.5 billion

- Net Income of $21.6 billion

- Earnings per share of $5.0

- Total assets valued at $1.9 trillion

- Market Cap at $186.4 billion

- A workforce of 247,850 employees

- Over 5200 branches and 13000 ATMs in the US

- Stock price of $48.1 as of Dec 2021

- Market share of 12.5 percent in the US banking industry

Wells Fargo is one of the few financial companies to have not only survived but thrived over 150+ years. Over this considerable timespan, the company underwent numerous structural changes and has weathered through tough situations, becoming stronger than ever.

Let's take a closer look at Wells Fargo's journey to understand how it became the 3rd largest financial services provider in the US.

Humble Beginnings: How did Wells Fargo start?

Wells Fargo is a renowned banking institution today, but this wasn't always the case.

In fact, William Fargo and Henry Wills started the company in 1852 with the primary intention of providing express services from the Philadelphia mint. These two individuals were also the founder of the famous company, American Express Railways.

The opportunity behind Wells Fargo

The Californian Gold Rush presented an opportunity for these two individuals to offer express and freight services to miners in the Californian region.

At that time, there were no railroads in California; hence, these two entrepreneurial geniuses tapped the opportunity and partnered with independent stagecoaches to enable the fastest delivery of gold dust.

The company also had a banking division, Wells, Fargo & Co Bank, which facilitated the purchase, sale, and transport of gold dust from the West to the East Coast via ship.

The business boomed, allowing Wells Fargo to expand its staging business and help develop a new company, Overland Mail, in 1957.

Overland Mail operated on the Pony Express route, and Wells Fargo was its primary lender. However, things took a turn in 1960 when Overland Mail defaulted after a failure of the Congress Bill.

How did Wells Fargo Expand Its Staging Business?

After the foreclosure of Overland Mail, a grand consolidation took place in 1966, which brought all the Western stagecoaches, including Holladay lines, under the sole ownership of Wells Fargo.

Wells Fargo was the unrivaled leader of transportation in the West, and it was also the time when the famous stagecoach icon/logo came into existence.

However, the stagecoach business started failing after the completion of the transcontinental railroad in 1969. Wells Fargo tackled this situation by shifting to freight transportation and establishing its own transcontinental express with access to dozens of railroads.

The result? Wells Fargo could access the profitable East Coast markets and serve over 25 states. During this time, the company also changed its name from Wells, Fargo & Company to Wells Fargo Company.

At the turn of the century, Wells Fargo had over 3500 express and banking offices.

.jpg){kind=link}

Key Takeaway 1: Address Your Competition Before It Takes Over You

William Fargo and Henry Wills were visionaries, and their ability to ascertain the demand for a specific service allowed them to benefit from an opportunity that reaped the rewards for years to come.

However, the most surprising part was that these leaders never underscored their competition. The prime reason for Wells Fargo success was that both owners focused on expanding the staging business to untapped areas.

This explains why Wells Fargo acquired operations of its biggest competitor, Holladay, in 1966. But that's just not it!

The company quickly realized the declining roots of the staging business and shifted to different transportation methods, i.e., freight and railroad. As a result, the company gained market control of almost 25 states and 2500 communities. A tremendous feat in the ancient age, isn't it?

Wells Fargo Focuses on growing their Banking Subsidiary

In 1905, the banking operations were finally separated from the express business, with the latter being acquired by Railways Express Agency (REA) in 1918.

The growth of Wells Fargo bank accelerated in the 20th Century, followed by an outrageous series of acquisitions and the adoption of contemporary banking methods.

How did Wells Fargo Expand its Banking Business?

Wells Fargo corporate strategy involved the expansion of business through mergers and acquisitions.

In 1905, the bank merged with Nevada National Bank to expand its operations in other territories. To further widen its base, Wells Fargo merged with Union Trust company in 1923 and the massive American Trust Company in 1960.

Wells Fargo attempted to establish its branches in various states, but it didn't happen until 1968 when it became a federal banking charter – a facility that allowed Wells Fargo to set up businesses for different banking services such as equipment leasing and credit cards.

The bank completed a series of acquisitions in the same year, with Sonoma Mortgage's $10.8 million stock purchase being the famous one.

Finally, Wells Fargo holding limited was established in 1969, and Wells Fargo bank was its primary subsidiary.

What was Wells Fargo's Strategy in Retaining its Position During the 20th Century?

Wells Fargo was always one step ahead in adapting to the new technologies in the banking industry.

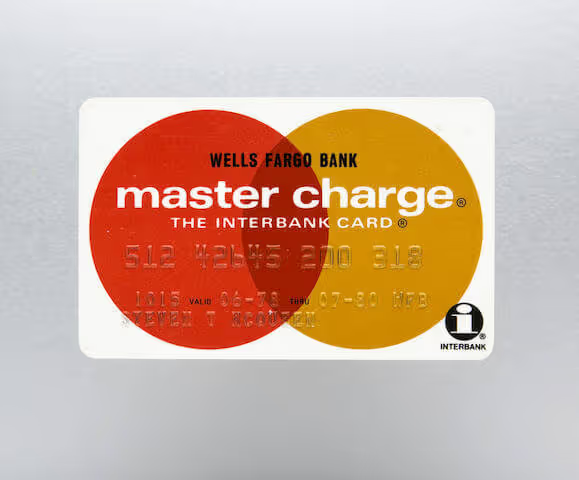

For example, Wells Fargo, along with three other banks, introduced a Master Charge Card, now prominently known as Mastercard, in 1967 – which proved to be a profitable move.

Furthermore, Wells Fargo established a global presence through acquisitions and partnerships with a wide network of affiliates and retail branches.

For instance, the bank made well over ten acquisitions between the 1980s and 1990s, including:

- Crocker National Bank in 1986

- Personal trust business of Bank of America in 1987

- Barclays Bank of California in 1988

- Over 130 branches of Great American Bank in 1991

- First Interstate Bancorp in 1996

All these acquisitions, especially the Crocker Bank one, helped Well Fargo to conquer the South Californian market and increased its consumer loan portfolio by over 85%.

Let's not forget that Wells Fargo was the first to establish online banking in 1995, further boosting the customer experience. In addition to this, the bank entered various financial services segments, including the brokerage business, by segmenting with Nikko securities in 1989, increasing its services offerings.

Why did Norwest acquire Wells Fargo in 1998?

By 1997, Wells Fargo was the 10th largest bank in the US, with total assets valuing over $88.54 billion. However, its recent acquisition of Interstate Bancorp wasn't well planned, and Wells Fargo had to suffer from lost customer deposits and a few bounced cheques.

To prevent the situation from worsening, Wells Fargo decided to merge with Norwest – the 11th largest bank in the US with a net income of $1.35 billion.

Norwest services were offered in all fifty states, and it had an excellent customer base in Texas, Minnesota, and Colorado. On June 8th, 1998, both these giants announced a 'merger of equal' in a stock deal of $34 billion – the step that created one of the most diversified financial services networks under the Wells Fargo brand name.

Key Takeaway 2: Acquire established players to expand into new markets

Throughout the 20th Century, Wells Fargo has focused on expanding its customer base and penetrating new banking services through mergers and acquisitions.

For example, the Crocker bank acquisition in 1986 is the perfect example that helped Wells Fargo diversify their services into Southern California and increase its consumer loan services. Moreover, Wells Fargo was one of the first banks to introduce credit card services in 1967, which significantly accelerated its net income.

In addition, Wells Fargo has been trying its best to set up regional branches/subsidiaries since 1960. Finally, it got the federal charter after eight years, expanding its operations across the US.

Nevertheless, the numerous acquisitions and expansion into new markets helped Wells Fargo survive throughout the 20th Century and the "merger of equal" decision by the turn of the Century proved to be a fruitful step.

Wells Fargo’s Growth in the 21st Century

Wells Fargo didn't stop expanding even after merging with Norwest. In fact, the growth that followed the "merger-of-equal" was fast-paced, with Wells Fargo acquiring numerous financial organizations offering different services.

{kind=link}

How did Wells Fargo Expand its Business Post-Merger?

As part of Wells Fargo positioning strategy, the company continued to acquire small financial companies and grow its accumulated assets.

In 1999 alone, Wells Fargo acquired over 13 financial companies with an accumulated asset valuation of $2.4 billion.

But the expansion didn't stop there. In 2000, Wells Fargo expanded its retail banking business in two more states: Michigan and Alaska, by acquiring Michigan Financial Corporation and National Bank of Alaska, respectively.

In the same year, Wells Fargo contracted its most significant deal of $3 billion in stock for First Security Corporation, a $23 billion financial holding company with operations in seven western states.

By 2003, the aggregate list of takeovers included 22 banks, 12 consumer finance companies, four security brokerages, 17 insurance brokerages, and several other small acquisitions.

Simply put, Wells Fargo was a financial giant in the West by 2003. However, it shifted its focus to penetrating new financial products and offerings, including mortgages, servicing contracts, and securities trading.

The Prominent 2008 Wachovia Acquisition

The expansion slowed after 2003, and Wells Fargo focused on developing its various banking services while improving the customer experience.

In 2007, the bank again acquired several financial companies, including Greater Bay Bancorp and CIT Group's construction unit.

However, the big opportunity came in 2008 when Wells Fargo bid $15.1 billion to acquire a troubled yet high potential bearing corporation, i.e., Wachovia bank.

Wachovia suffered from a mortgage meltdown since many of its customers were defaulting on loan payments; hence, several prominent players were eyeing to acquire it. However, things were smooth for Wells Fargo. A court injunction was issued to prevent the transaction since Wachovia was already underway in negotiations with Citibank.

The Court overruled the injunction, and Citigroup was given a chance to enter negotiations with Wells Fargo. The negotiations failed, and Citigroup was unable to prevent the merger.

Finally, the merger was approved on 12th October, and Wells Fargo was able to expand its operation into nine Eastern and the Southern States. This merger was a turning point for Wells Fargo, creating a super-bank with $1.4 trillion in assets with 48 million customers. In addition to this, Wells Fargo was able to add international offices of Wachovia in its wings after the merger.

How did Wells Fargo Survive Through the 2008 Financial Crisis?

Wells Fargo was one of the few giant US banks able to absorb the catastrophic effects of the subprime mortgage crisis in 2008.

Although there was a dip in the profit margins of Wells Fargo, the bank remained afloat during the crisis. Here's how:

FEDs Support

The FED conducted stress tests for the bank to identify the minimum capital requirements to withstand the crisis storm. And so, Wells Fargo received a $25 billion Emergency Economic Stabilization Act Federal bail-out in the form of a preferred stock purchase.

Furthermore, the bank announced a stock offering to raise capital to subdue unforeseen circumstances. The additional capital was raised partly through retained earnings or stock offerings.

Diversification

Wells Fargo business model focused on selling financial products to a diverse cohort of borrowers. The lending system was designed to lend not only to real estate borrowers but also to small businesses, auto loan borrowers, and energy and agriculture industries.

Setting of Provisions

Wells Fargo's corporate strategy for dealing with such situations was simple yet effective. The bank consistently set aside money reserves at the beginning of the crisis to absorb losses in lending. During 2008-2009, the bank recorded provisions of $42.6 billion, while the write-offs were $29.5 billion.

There are two benefits of this strategy. First, the first-year profits of Wells Fargo will bear the shortfall caused by the crisis. Secondly, it can boost its earnings in later years by releasing provision balances.

This strategy helped Wells Fargo remain afloat while other giants were receiving legal notices of bankruptcy.

After-effects of Financial Crisis 2008 on Wells Fargo

The 2008 financial crisis undeniably created a bank run and rippled the financial sector. Although Wells Fargo absorbed the effects of the crisis, the bank slowed its expansion policy and instead pursued penetrating new banking services.

Therefore, the bank started its investment banking division in 2009 by establishing another subsidiary, Wells Fargo Securities. The subsidiary was created to house new capital market groups acquired by Wells Fargo during the Wachovia merger.

This was a significant step since Wells Fargo has little to no prior experience in investment banking, and this move boosted Wells Fargo’s revenue.

Shortly after, the bank focused on developing other banking divisions by acquiring North Coast Surety insurance services in 2009 and Merlin securities in 2012. Furthermore, Wells Fargo hired 25 investment banking professionals from Citadel LLC to strengthen its investment banking division.

Similarly, Wells Fargo acquired GE capital rail services, and three GE units focused on business loans for equipment financing in 2015.

For the rest years, the bank followed a similar growth strategy and strengthened its various banking divisions through small mergers and customer experience enhancement.

In 2020, the bank even ranked #30 in the list of Fortunes rankings for America's top corporations.

Key Takeaway #3: Assess and Mitigate Risks Before It's Too Late

One thing is clear: Wells Fargo did a commendable job surviving the impact of the most destructive financial crisis.

Most strategic banks' earnings took a hit and plunged into deep waters during the crisis. But that wasn't the case with Wells Fargo. The company not only survived but also expanded its operation by merging with Wachovia corporation.

Wells Fargo's business strategy to deal with crisis imparts a valuable lesson: always assess and diversify risks and make provisions for them earlier. In this way, the corporation is prepared to take the brunt of the crisis's repercussions and move on. It's not the first time that Wells Fargo was successfully able to survive the crisis, but the bank applied the same strategies to survive through the 1991 financial crisis.

Wells Fargo’s Digital Transformation Strategy

To stay relevant during the 21st Century, every giant corporation has undergone a digital transformation.

Wells Fargo, a corporation operating for 160+ years, has been proactive in adapting to the digitalization of its infrastructure and delivering incredible digital experiences to its customers.

In fact, Wells Fargo was the first bank to adopt internet banking in 1995 – way before internet usage became mainstream.

Wells Fargo Launches its Retail Banking Application

Although Wells Fargo rolled out their online money management system in 2005, the bank introduced its first retail mobile application in 2012, with additional resources such as alerts and notifications.

The introduction of the mobile application allowed users to manage accounts, transact, and explore financial products – all from the confines of their homes.

Over the years, Wells Fargo has improved its mobile application's layout, design, and user-friendliness, and it's expected that the bank will add a virtual assistant feature with the name "Fargo." This excellent feature will generate quick responses to user queries and provide insights to customers regarding better financial management.

Mobile-Based Contactless Transactions Are Here

With the advent of mobile wallets like Apple Pay, Wells Fargo didn't delay announcing a plan for smartphone-based transactions.

In addition to this, Wells Fargo initiated the facility of cardless ATMs, enabling users to withdraw cash using Wells Fargo app. The best part is that this service is accessible at 13000+ ATMs.

While we are talking about card payments, Wells Fargo rolled out two new credit cards, Active CashSM and ReflectSM, in 2021, which provide cashback rewards for on-time payments. All these new services have increased the rate of digital card activation and enrollment in paperless transactions.

Wells Fargo Lab and The Control TowerSM

Wells Fargo has, over the years, focused on improving the user experience and so launched the Wells Fargo Lab – an innovative strategy which gives users a platform to voice their opinions and suggestions about digital facilities.

In addition, the Wells Fargo innovation Lab is helping entrepreneurs set up innovation labs to create advanced technologies and improve digitization. By doing this, the bank aims to build relationships with such individuals and partner with them somewhere in the future where their technologies can be advantageous to the bank.

Let's not forget about the control tower – a digital experience allowing customers to manage their digital financing footprint from a single location. In addition, the control tower feature enables customers to stop recurring payments (if any) with just a few clicks.

Wells Fargo Partners Up with Google and Microsoft Azure

Wells Fargo has selected Google and Microsoft Azure as their public cloud providers as part of their digital infrastructure strategy.

Microsoft Azure is expected to act as the primary cloud provider, while Google provides additional business-specific cloud services. The partnership will create innovative solutions, enhance user experience, and increase workplace collaboration.

The analytics and data sources will dig deep into customer records and provide personalized customer service.

Key Takeaway #4: Adopt new technologies to gain an advantage

Wells Fargo was among the first banks to initiate internet banking and facilitate its customers. Today, the corporation is driven to reduce its branch footprint through its mobile technologies.

The bank is moving to a cloud-based platform to understand its user needs further and amplify user experiences. On the other hand, they have launched a portal to listen to customer suggestions and improve.

Hence, it can be extracted from the Wells Fargo growth study that the key to surviving for more than 160 years is to assess customer demands and fulfill them to stay on top.

Why is Wells Fargo So Successful Today?

From starting as an express business to becoming one of the top financial giants in the US, Wells Fargo has come a long way.

What Is Wells Fargo’s Competitive Advantage?

Wells Fargo offers a diversified range of services to cater to a wide consumer base.

From serving college students to businesses and from doing retail banking to community banking, it manages it all through its four business segments, including Consumer Banking and Lending, Commercial Banking, Corporate and Investment Banking, and Wealth and Investment Management.

What Is The Business Model of Wells Fargo?

Wells Fargo generates revenue mainly through commissions and fees on its various private, consumer, and commercial banking services.

Wells Fargo is renowned for being the first bank in the US to offer online banking services. It continues to set the bar higher in terms of digital innovation and delights its wide consumer base.

Who Owns Wells Fargo Today?

Wells Fargo & Company is a holding company with financial subsidiaries, with Wells Fargo Bank being the primary one.

Wells Fargo & Company shares are traded on the NYSE, and Berkshire Hathaway owns 10% of the company's shares.

What Is Wells Fargo's Mission?

Wells Fargo's mission is to make customers financially independent.

"Helping customers succeed financially."

What Is Wells Fargo's Vision?

Wells Fargo's vision is to match customers with desired financial products to help them achieve their dreams.

"To satisfy our customers' financial needs and help them succeed financially."

Wells Fargo’s Growth by Numbers

Here are the key lessons extracted from the expansive journey of Wells Fargo.

Increase Market Share Through Acquisitions

From the first merger with Nevada bank to the acquisition of Wachovia Bank, Wells Fargo has followed a strict expansion strategy to penetrate new regions and increase its market share.

Just between 1990 to 2003, the company acquired well over 30+ financial institutions and established its dominance in the West.

But the key lesson is that Wells Fargo acquired banks with already established markets. Hence, the company didn't have to do much groundwork to develop a related-party corporation.

Focus on Diversifying Risks

Of course, Wells Fargo did expand its customer base through countless acquisitions, but the bank didn't put all its eggs in one basket.

We simply mean that the bank didn't only acquire financial institutions, but it took over insurance companies and security brokerages, and even established an investment banking division, among other ventures.

Furthermore, the bank targeted numerous groups within these divisions and didn't limit itself to a single segment.

That's one of the prime reasons why the bank survived the raging effects of the 2008 global financial crisis. Secondly, establishing different banking divisions allowed the bank to boost its growth and net income over the years.

Know Your Competition Inside Out

Since its inception, Wells Fargo didn't overlook their competition. In 1866, the express business took over all the Western stagecoaches and became the unrivaled leader in the transportation industry.

If we talk about the banking division, Wells Fargo acknowledged its competition and the impending future challenges. It explains why the company was proactive in acquiring its competition, Crocker bank, in the 1980s.

Oh, and the visionaries behind Wells Fargo had ascertained the digital advancement way before it took over the world. It's also one of the reasons why the company was the first to initiate MasterCard and set up internet banking in 1995 – which proved to be a fruitful step in improving its profitability.

Over the expansive journey of 160+ years, Wells Fargo has survived countless roadblocks and paved the way to becoming the fourth largest financial institution in the US. Wells Fargo's vision, business model, acquisition plan, and sheer will to improve customer experience have allowed the business to grow and maintain its unparalleled reputation.