Zurich Insurance LTD. is a Swiss insurance company headquartered in Zurich, Switzerland, with operations in 6 continents and a significant concentration in Europe, North America, and Australia.

Founded as a marine reinsurer in 1872, Zurich Insurance provides a wide range of property, casualty, and life insurance products across the globe.

Its business is subdivided into three core branches, namely: “Global Insurance,” “Global Life,” and “Farmers” and its customers range from individuals and SMEs to large organizations and MNCs.

Here are some recent facts and statistics from 2020 that highlight the growing stature of Zurich Insurance:

- Total revenue of $51.6 billion

- Business operating profit of $4.2 billion

- Market capitalization of CHF 56.2 billion

- Return on Equity of 14%

- Over 55,000+ employees

- Customers across 215 countries and territories

- Share price of CHF 373.5 as of Dec 2020

Now, let’s review the incredible journey of Zurich Insurance, full of trials and tribulations, right from its humble beginnings in the 19th century to today!

From Marine Reinsurance To Building Financial Strength

Founded as “Versicherungs-Verein” (Insurance Association) in Zurich in 1872, Zurich Insurance started off as a subsidiary to the parent company “Schweiz” - a big name in the marine insurance industry.

Global Since The Start With Schweiz

Towards the end of 19th century, as developments in the fields of safety, services, and engineering were made, opportunities in the insurance industry grew considerably.

Subsequently, in 1875, Versicherungs-Verein entered the accident insurance arena while working as a subsidiary to Schweiz. At this point, it rebranded itself as “Zurich Transport & Accident Insurance Limited.”

The company benefited from opportunities that arose due to a change in the legal environment of Germany when improved jurisdictions were introduced. These laws made factory heads responsible in case of accidents in workplaces. This also paved the way for Zurich to expand its official presence in Germany, Austria, Denmark, Sweden, and Norway.

Expansion Within Europe

Still, under the Schweiz tag, Zurich continued its expansion within Europe. In 1877, it opened an office in Brussels, Belgium. Later, branches in Almelo and Paris were inaugurated.

With its landscape and market horizon expanding, Zurich jumped on to the opportunity to facilitate the growing middle class of that era. Thus, in Germany, it started introducing a micro-insurance that covered low-income consumers.

Zurich worked with a core principle of “No business without a sufficient premium” to gather its stakeholders and even argued with its parent company over it. Within a short span of time, it yielded positive results.

Exit From Marine Business

Working alongside Schweiz became difficult when a heavy loss was incurred around 1880. Thus, Zurich immediately left the marine insurance business while covering its loss using capital reserves and appointing Mr. Heinrich Muller as its CEO.

Muller tackled the turnaround as he focused on casualty insurance and dividend cuts to pump the premium incomes to 1 million CHF.

Understanding Markets And Risk Engineering

By 1881, Zurich figured out its key markets with the biggest share coming from Germany followed by France and Switzerland. These 3 states alone made up 94% of the business while the rest was coming from Austria, Belgium, and Scandinavian states. The company also made its way to Italy in Milan.

Now, Zurich’s managers and official personnel started talking about worker protection via proposals in the production industry. This was the dawn of risk engineering where the firm stood out by ensuring additional risk management and providing on-point advice in production to minimize any unforeseen events.

Zurich dealt with a catastrophe claim in 1883 in France while making sure it followed its laws fairly to satisfy all its stakeholders.

Political Innovation And Expansion To Russia And Spain

The company penetrated into the Russian market via agents spread across Moscow and Helsinki. Furthermore, an agency was set up in Barcelona in 1884 as well to complete the first turn of international expansion.

In 1886, Zurich’s profits in Germany fell for the first time when the compensation laws were nationalized. Here, the company took a politically informed step by covering the loss from Swiss and French markets and introducing liability insurance in Germany. This new product covered many liabilities from horse owners to medical and real estate, thereby considerably expanding their target consumer base.

Renaming, Expanding, And Financing

In 1894, the company took the name “Zurich General Accident & Liability Insurance Limited.”

In the years that followed, with new insurance laws for workers around Europe, Zurich capitalized on the market, focusing primarily on France around 1900. Very quickly it became the largest casualty insurer in France.

Fritz Meyer replaced Muller in 1900. Meyer focused on building financial strength and was called “Reserves Meyr.”

Key Takeaway 1: Independence & Leadership Matters

From 1872 to 1900, Zurich Insurance underwent significant organizational changes, international expansion, and rebranding.

It successfully navigated through challenging legal environments and the market landscape through exemplary leadership that made its customers, shareholders, and employees the top priority. At the same time, it kept following its north star of internalization and financial independence.

As a result, the company became one of Europe’s most prominent insurance providers within a few years.

Into the New World and Market Positioning

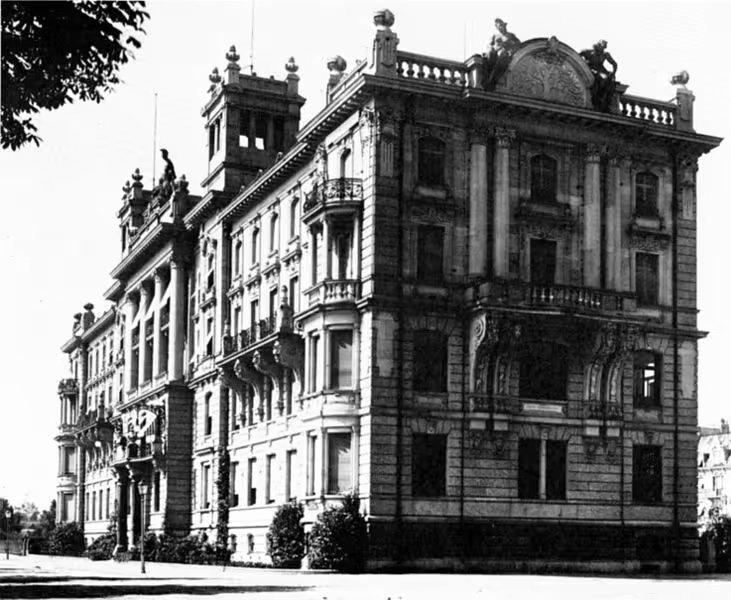

Zurich Insurance’s iconic head office in Mythenquai was unveiled in 1901. The company was praised for its architectural art. Even weekly chronicles and business magazines around Europe wrote about it, providing a further boost to the company.

The new office was considered equivalent to Zurich’s reputation in the industry, highlighting its dominance.

_1905.jpg){kind=link}

Into the New World

Belgium and Italy introduced new laws in 1905, resulting in a prompt response from Zurich’s managers. They made amendments to Zurich’s policy for private insurance to workers saving the company from losses and securing the method to check risks.

Few years later, with the assistance of a veteran employee, Leonhard Tobler, Zurich landed into the US market in December 1912.

The American market was a booster shot to Zurich’s entire premium income starting off with 9% share in the first year. Fast forward to 1920, the US made 50% of the company's gross premium.

Tobler’s timely decision benefited Zurich amid World War I where the company went an extra mile to facilitate its customers - turned into prisoners of war - via its international networks.

First Acquisition and World War I

On the other hand, during the war, Zurich went for its first acquisition of “Hispania Compania General de Seguros” in 1915. The company bought the stocks of Compania General in times of financial crisis at discounted prices.

Again, exploiting the opportunities in war times, Zurich understood the market and engineered new products. In 1917, war promoted the idea of “accident insurance for soldiers serving the front”. Following the same stance, another product was launched for insurance against mine and bomb accidents.

International Expansion With New Products

With its competitors busy in local markets, Zurich utilized its financial strength and expanded into the British market in 1922, becoming the first foreign insurer in the country.

The company also launched the “VITA Life Insurance Company”. This step enabled Zurich to absorb bankrupt French and German companies of Swiss origins. VITA went as far as to make its separate chain across Europe.

Simultaneously, in 1922, Zurich focused on a third avenue and introduced new products covering sureties and children. In 1923, Zurich inaugurated a branch in Canada covering the entire North America.

Acquisitions, Ford, And Medical Check-ups

Leonhard Tobler was appointed as the CEO in 1924. His era featured several major acquisitions, including Lancashire and Cheshire Insurance, UK (1924), Kosmos Insurance, Austria, and Deutsche Allgemeine Insurance, Germany (1928). In 1929, the company also set up Zurich Fire Insurance Company in New York.

Zurich also partnered with Ford in the UK. With Ford’s trust and position in the market, the company made more than 60,000 pounds out of this scheme. This premium income made for up to 50% of Zurich’s entire earnings from the UK.

VITA penetrated the European market, turning Zurich the pioneer of providing free medical check-ups to its stakeholders. By the mid-1930s, this product included preventive surgeries and by 1968, healthy lifestyle courses were introduced as standards.

Economic Crisis And Dawn Of Leveraging Data

Wall Street crashed in 1929, resulting in a global economic crisis and the dawn of a new era for Zurich.

In 1930, Zurich bought Merkur Insurance in Prague. In 1935, it acquired Bedford Insurance, UK, and Holmia Insurance, Sweden.

Back in the headquarters, Zurich started with electronic data processing in the 1930s. Fifty-eight years after its foundation, Zurich’s accounting and controlling data was being converted into punch-card machines.

Positioning In The Markets

Zurich was declared as a leader in liability insurance in 1933 in Chicago adding to its market dominance and trust. It also started focusing on the emerging market segment of women. A special accident insurance for women was introduced in 1935 to accommodate the company’s stance.

Zurich also introduced its “Safety Zone Program'' targeting insured factories. With another world war looming, the company focused on the defense sector, especially in this program.

Its market position boomed post World War II as the west started funding businesses in war-ravaged states. By 1946, Zurich boomed with exemplary gross premiums reaching as high as 74% in European markets.

Key Takeaway 2: Financial Strength Helps Navigate Crisis

From 1901 to 1950, Zurich Insurance’s financial strength and international outreach helped it to endure a global economic crisis and two world wars. Its strategy of buying companies in trouble at discount rates to restructure them was powerful enough to change the market landscape.

Zurich’s growth in these hard times was exemplary as compared to its competitors at that time, and this set the stage for it to conquer the insurance industry in the times to come.

Becoming The Zurich Insurance Of Today

Zurich tapped into the African market for the first time when a branch office was set up in Casablanca, Morocco in 1951. This step was a landmark towards Zurich’s greater goal of declaring itself as a one-stop wholesale insurance entity.

Expansion Across Five Continents As A Multi-line Insurer

Following its old strategy to acquire companies at a discount, Zurich completed the acquisition of the Australian Commonwealth General Assurance Corporation in 1961. The company had landed in the 5th continent.

By now, it was known as “Zurich Insurance Company” in accordance with the multi-line insurance products it offered across the globe.

Zurich also entered Latin America in 1965 using its tried and tested strategy of acquiring companies, including Alpina Insurance. The move also allowed the firm to reenter the marine insurance sector.

From Corporation Insurance To Moves in Asia and America

In 1975, Fritz Gerber appointed Rolf Huppi to lead an international division for the company’s expansion plans. This also meant Zurich was the first insurer in the European Union to offer Umbrella programs for its corporate clients. This turned out to be a foundation of Zurich’s major success with its evolved form as “Global Corporate” segment today.

Risk engineering was not given much importance in the European market by 1978, especially for corporations. Zurich entered into this niche and started off with “Zurich Hazard Analysis”. The international division started providing integrated risk analyses to its corporate clients going beyond traditionally analyzed property risk to include safety and liability risks. This value-addition built exceptional trust for Zurich in the market.

The company also laid foundations in Hong Kong in 1973. In other parts of Asia, Zurich started a joint venture with Malayan Group, a big market player based in the Philippines. At this point, Zurich tapped into non-life insurance in this market based on its research.

Meanwhile, Zurich Reinsurance New York was founded after successfully acquiring Fidelity and Deposit with partner Swiss Re.

Altstadt And The Biggest Takeover

Zurich kept an eye on customers and competitors simultaneously. Altstadt had come to Switzerland in 1959 and was a threat to one of its major markets. Eliminating the threat, Zurich brought Altstadt in 1982.

In 1984, a major acquisition was done in Sao Paulo, Brazil, cementing its position in Latin America. Soon after, in 1986, Zurich acquired the license to operate in Japan too.

Then, in 1989, Zurich completed its largest takeover to date - the Maryland Casualty Group for $740 million - leading to an almost doubling of the company’s revenues.

Return To Russia

After the dissolution of the Soviet Union and the emergence of new markets, Zurich re-entered Russia in 1996, 111 years after it had done so for the first time by acquiring a 49% stake in the industrial insurer Westrosso.

Zurich realized the Allfinanz concept by acquiring over 80% of Kemper Corporation, with two life insurance subsidiaries and 97% of Kemper Financial Services.

Simultaneously, the company founded Zurich Capital Markets to focus on alternative financing and derivative business transactions.

It also acquired a majority interest in a purely financial non-insurance company for the first time: Scudder, Stevens & Clark, New York. Subsequently, the Kemper activities were merged into Scudder to form Scudder Kemper Investments, later renamed Zurich Scudder Investments.

Reaching For The Stars

Zurich rebranded itself as “Zurich Financial Services” in 1998 after its major strategic move to combine its financial business in the UK (B.A.T industries) and US (Farmers Insurance) under one umbrella.

This merger allowed Zurich seamless collaboration as its presence across continents became uniform. The employee count doubled from 30,000 to 60,000 as Zurich celebrated its 125 years of success.

Aligning For The 21st Century

With the start of the 21st century, Zurich started refocusing its value proposition internally and externally. James Schiro of PriceWaterhouseCoopers was appointed as the CEO in 2002, breaking the tradition of appointing CEOs from the company executives.

Schiro aligned the company’s focus when he saw a steep drop in Zurich’s share price. He brought back attention to the core business of insurance finance and sold or merged the non-core businesses. Plus, the company divested from all international operations not meeting the minimum thresholds of profitability.

Furthermore, Zurich strengthened its capital and introduced a KPI of business operating profit to track its goals.

Zurich presented its new face to the world as a sustainable brand by delivering exceptional service to its customers during Hurricane Katrina and Wilma in 2005. Despite the enormous claims linked to these events, Zurich remained profitable due to its market trust.

So much so that in 2006 Zurich reported a record operating profit of 5.9 billion USD along with a 19% return on equity.

CSR And Customer Relationship Management

With its operating profit as high as $6.6 billion by 2007, Zurich established global initiatives to take on some of the century’s most pressing challenges: poverty, through its Microinsurance Practice; and climate change, through the Climate Office.

Zurich navigated the financial crisis in 2008 with its care and discipline. Stakeholder trust helped the company deliver positive results and a solid investment return. Zurich HelpPoint was introduced as a common denominator for the company’s many advice, service, and solution offerings for its customers.

Zurich closed 2009 with its 28th consecutive quarter of profitability. The balance sheet remained strong and solvency margins were at near-record levels.

Rebranding and Global Reach

By 2010, Zurich reached two notable milestones in its selective emerging market expansion. The first is the acquisition of Malaysian insurer Berhad. The long-term alliance with Banco Santander is the second milestone, under which Zurich can reach a potential 36 million customers in Latin America with its general and life insurance solutions.

In 2011, Zurich celebrated its one-hundred years of helping customers understand and protect themselves from risk. Zurich changed its name from Zurich Financial Services to Zurich Insurance Group in order to more accurately reflect its business and the role the company plays in society.

In 2015, Zurich became the first global company in the insurance industry to be certified by ‘EDGE’. Zurich is making progress in creating a diverse environment that brings out the best in Zurich employees and attracts the brightest talent.

From 2016 Onwards To Today!

{kind=link}

The year 2016 marked a turning point for Zurich as it announced a planned structural change of ZIC group to eliminate complexities and create a simpler and more customer-oriented structure to support global and local businesses. The company tinkered with various structures before finalizing one by the year-end. It enhanced the focus on geographic regions in the core businesses and merged the corporate and commercial business into a single global business

2017 was a year of action. In its quest to expand its services and adapt according to the changing customers' needs and preferences, competition, and digitization, Zurich acquired a number of companies, including ANZ’s Australian life insurance arm OnePath Life, the leading travel insurance services provider, Cover-More, and Bright Box, a global telematics solutions provider.

Having reshaped its business and buckled up for difficult yet necessary transformation, Zurich further invested in embracing a customer-led technology-enabled transformation. At the beginning of the year, Zurich launched its flagship ‘Make the Difference’ program inviting employees to help propose how to improve the workplace. The company also acquired the Latin American operations of QBE, becoming the largest insurer in Argentina, EuroAmerica's life businesses in Chile, and a majority stake of Adira Insurance in Indonesia. It also launched a competition for startups to look for and promote quality customer solutions.

In 2019, Zurich set up a Customer Office to focus solely on surpassing customer expectations and delighting customers at every touch-point with the company. It also focused more on retail expansion on the back of innovative and adaptable products and services, such as the Zurich klinc on-demand gadget insurance in Spain, and ToggleSM, customizable insurance with innovative services for renters, introduced by Farmers in the U.S. The company also doubled down on making a positive impact by signing up for the UN Business Ambition for 1.5˚C Pledge, enabling employees to adapt to the changing times, and ensuring trust remains entrenched in the company by issuing personal data management commitment to customers.

#ZurichNeverStops was the hashtag that trended in 2020, highlighting the company’s commitment to caring for its customers, communities, and the planet. The company ramped up its digitization measures in line with the ‘new normal’ and provided a robust and resilient response amidst the Covid-19 pandemic. It launched a variety of new products and services such as the LiveWell well-being unit and acquired MetLife’s property and casualty business.

Key Takeaway 3: Global Expansion Demands Mergers, Acquisitions, And Better Internal Control

Over the past 70 years, Zurich went through various cycles to declare itself as an exemplary multi-line global insurer. From expansion across 5 continents to a long list of acquisitions and mergers, Zurich set a bar for the players in the market. Plus, it took bold decisions such as making structural changes in 2016 to turn the business around and become future-ready.

Fast decision-making and organizational control along with global financial strength saved Zurich even during the worst economic crises. Zurich’s customer experience, sustainability goals, and “be there when you need” strategy earned it the market trust. Enhanced internal management and employee experience kept the organizational flow strong enough to deal with external challenges.

The Business Model & Strategy Of Zurich Insurance

{kind=link}

Zurich Insurance has continued to refine its business model over the years in its quest to do better.

To create value for its entire stakeholders, the multi-line insurer is making efficient use of its resources, including financial capital, intellect, people, society, and key relationships with relevant stakeholders.

Business Strategy Driving Growth

Remaining true to its vision and mission, Zurich Insurance’s strategy is to play on its strengths to achieve organizational success. A nuanced people-driven brand trust and strong financial position are pertinent to Zurich’s balanced strategy. Its main preferences include:

Customers

Zurich is still on its way to evolve into an entirely customer-driven organization. During the COVID-19 pandemic, it deployed quick customer channels under its “Global Business Platforms” unit to digitally satisfy customers' needs. It is also trying to align with its current and prospective customers (Millennials and Gen Zs).

With changing market landscapes post-pandemic, Zurich is working on a multi-faceted customer strategy in digital environments. A roll-out of “Brand Visual Identity” is underway to connect with customers emotionally while meeting their future expectations.

Simplification

Insurance seems complicated at first glance, but Zurich is efficiently using its resources to run its successfully simplified business.

For example, Zurich formed a digital strategy to cut the assessment time from 10-15 days to 15-30 minutes in claim assessments. This rapid simplification happened with the advent of a smartphone app incorporated into Zurich’s business.

The company sorted everything simply from digital signatures to internal data management during the lockdowns. It is still simplifying its front-end while working on digital products for SMEs.

Zurich’s future strategy is also automating core insurance tasks across different geographies, customer groups, and business lines.

Innovation

Customers have ever-changing attitudes making it compulsory for Zurich to adapt, meet, and exceed customer expectations and wants. Zurich’s digital strategy for its commercial customers has been successful with its innovative risk services.

It launched its “Customer Active Management” unit to understand customers for innovating services accordingly. Zurich involves new ideas via its programs and product offerings such as LiveWell and Zurich Innovation Championship as multi-line insurance.

But understanding customer psychology is an evolving journey demanding Zurich to disrupt its business model and go digital to keep up with changes.

Key Takeaway 4: Clarity Guides A Business Forward

One of the best aspects of Zurich Insurance remains its high level of clarity regarding its goals and visions.

The company follows a set plan, with pre-decided KPIs and a business strategy for its growth. This has helped it maintain an upward trajectory, while achieving its milestones timely. It also continues to modify its goals by adapting to the changing industry. This has been seen in the form of an expanding employee base as well as diversification to attract its transforming clientele of Gen Y and Z.

The Urgent Need To Embrace Digitalization

In recent years and particularly after the outbreak of the COVID-19 pandemic, Zurich Insurance has shown immense potential to innovate and embrace digital solutions.

However, the company still has a long way to go to fully integrate technology into its processes and to truly leverage it to excel its business and delight its customers.

Also, with the rapid progress of technology in the insurance industry, as well as its overall use in general customer-seller interactions, Zurich will face several challenges if it does not manage to keep up. For starters, it can lose the consumer base it has spent years trying to build simply because its competitors could innovate and harness the power of technology before Zurich does.

Predicting The Unpredictable

Analyzing and anticipating risks is one of the most important functions of any insurance firm. However, a phenomenon that really always existed but was brought to the attention of the whole world following the pandemic, is that many risks are too complex in nature to be accurately predicted without very advanced systems.

For instance, COVID-19 had a significant impact on people’s health outcomes and many insurance firms were struggling to cover the cost of increasing claims. In fact, behind the 9/11 attacks and Hurricane Katrina, this was the third-largest loss for insurers - totaling up to $44 billion.

With major global level changes, such as climate change, the rise of environmentalism, and remote work, international regulations on trade, risks for individuals and corporations both have become of uncertain nature. Yearly or long-term trends and predictions cannot account for these changes. Here the need is to incorporate fast-paced software that can analyze risks in real-time and provide measures by assessing all these dynamic variables.

Increasing Cyber Threats

Very recently, a Spanish Unit of Zurich Insurance fell prey to a cyber attack where hackers were able to break into customer data before being blocked.

Unfortunately, this is not merely a one-off instance of hackers attempting to breach financial companies’ cyber security protocols and obtain sensitive information. CNA Financial Corp, one of the USA’s largest insurance firms, lost a significant chunk of its data to a ransomware attack in 2021. Consequently, the company had to pay $40 million to recover its network’s control.

Such threats will only continue to increase in frequency and intensity; this being one of digitalization’s seemingly only downside.

For Zurich Insurance, this means that not only do they have to work on accelerating its operations, they need to do it fast and extensively. There is a major requirement to not just digitalize, but also invest in robust cyber security measures to counter these advanced threats and ensure the integrity of its information.

Digital Product Development

The 21st century has brought about a revolution in terms of how buyers and sellers interact. Although the insurance market wasn’t one of the first to embrace these digital interactions, it has gradually started to incorporate the idea.

Where plans and policies would take weeks or even months to formulate and formalize, the whole procedure of discussing a customer’s options, developing a customized package, and finalizing the words of agreements can be done completely digitally, within a matter of minutes.

Naturally, customers prefer the convenience and time-effectiveness offered via digital interactions and hence, opt out of tedious to and fro of in-person products.

If Zurich Insurance wants to keep its clients happy and loyal, it needs to offer a seamless digital experience and offer them a variety of flexible options.

Artificial Intelligence & Potential Loss To Competitors

The times have changed. While customers would not complain of standardized packages or strategies in the past, they have now begun to demand a tailor-built experience, and rightly so.

Many insurance companies have leveraged Artificial Intelligence (AI) to create unique products, develop personalized models, and use complex data methodologies to improve risk rates and pricing. With their customer-centric approach, they continue to attract a massive clientele because the people feel more than a mere ‘number’ in their list of consumers.

This puts Zurich Insurance at a disadvantage. While the company has identified a changing demand and approach for insurance products, the process to inculcate the findings remains slow. A rollout of ideas like “Brand Visual Identity” is a small step towards consumers, when the competition continues to be making strides in AI.

For Zurich to increase, or even maintain, its consumer base, there is an urgent need to digitalize and take it to the next level with personalized products that connect with consumers and aren’t based on a “one-size-fits-all” approach.

Key Takeaway 5: Success Lies In Adopting Digitalization

With rapid advancements in technology and competitors gaining their footing in the digital world, Zurich Insurance is in a difficult position.

Its success remains hinged on two factors: Stepping into technology and doing it fast.

Treading in times when the first to make a splash gains all attention in the consumer base, time is of the essence for Zurich Insurance as other insurers have already begun inculcating digitalization in their business models. Whether it is in the form of applications, cryptography, or the usage of AI in building client packages, they continue to gain momentum, while leaving Zurich behind.

Therefore, Zurich Insurance needs to act now, to retain and build its clientele, while also protecting itself from information hacks and unanticipated data leakages.

Growth By Numbers And Key Takeaways

It is difficult to imagine that the company we see as Zurich Insurance today actually began its journey in the 1800s. After numerous name changes, several acquisitions and mergers, and leadership transformations, it has transformed into an empire spanning 5 continents and with a legacy of 150 years.

Growth By Numbers

The company’s growth has been inspirational, and the numbers surely reflect it.

Note: As 2020 was particularly overwhelming for insurance companies with the unanticipated rise in claims due to the COVID-19 situation, its financial numbers would not truly reflect the remarkable growth Zurich has achieved in recent years. Therefore, we map its success from 2010 to 2019.

Key Strategic Takeaways

Develop A Strong Financial Mechanism To Withstand Difficult Times

Zurich Insurance has been a key player in the industry for over 150 years meaning it has survived through two world wars, the Great Depression, multiple global crises, and many more challenging circumstances.

In fact, many times, the company found opportunities to grow by acquiring other companies at discounted prices during global financial crunches. This was mainly due to the fact that the company smartly utilized its resources and always had a fair budget to fall back on when other companies were running out of funds.

Hence, rarely has the company faced a situation where it has had to bear more expenses than the revenue it has generated.

Develop A Global Customer Base Through Established Acquisitions

Throughout Zurich’s journey, the company’s go-to strategy for expansion has been acquisitions, be it the company’s penetration of any of its major markets.

This meant that even though Zurich had only just established its operations in a new region, it already had a set customer base left behind the company it had taken over.

Thus, it could cement its position much faster and rapidly and sustainably expand into five continents.

Never Stop Innovating

Progress is the stimulus of success, and Zurich Insurance has understood this fairly well by remaining anything but stagnant in its incredible journey.

The company’s tenure has included the “firsts” of many aspects; the first foreign insurer in Britain, the first to offer Umbrella programs in the EU, the first to acquire a non-insurance company, and so on.

This has meant that innovation remains one of the top priorities of the company to maintain an edge over their competitors while establishing a stronghold over their existing clientele.

While the innovation has yet to reach the digitalization route for the company, Zurich Insurance continues to identify changes and implement transformations to continue its upward growth.